Urgent repayment: high interest rates have shortened the mortgage of Russians

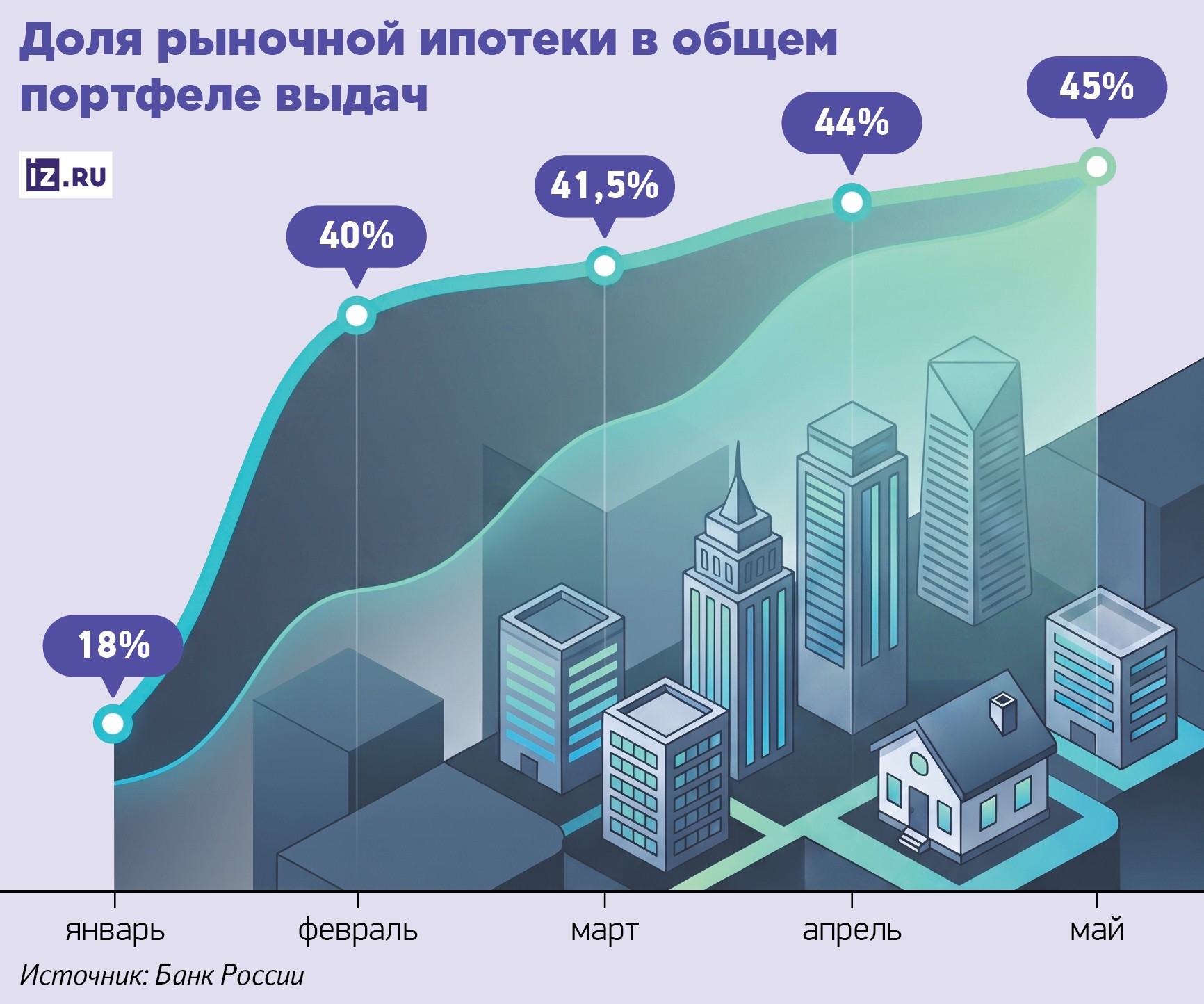

The average mortgage term has fallen to a minimum since 2022 — 23.5 years, according to the Central Bank. At the beginning of the year, it was 28.5 years old. The reason is the changing structure of the market. After the introduction of the "one preferential loan to one family" rule, issuance under the state program sank, yielding to market offers. Their share now stands at 45%, which is the maximum in two years. At the same time, a long mortgage helps the borrower less and less to overpower the loan. On a loan of 12 million, the difference between 30 and 25 years is only 1 thousand per month, but 10 million in overpayment. At what rates it is profitable to take out a mortgage and what to do if there is no right to benefits — in the Izvestia article.

Why did the mortgage term start to decrease

By the summer of 2026, the average term of new housing loans decreased to 23.5 years, the lowest level since 2022, according to the Central Bank. For comparison: Back in January, the figure was almost five years higher.

The reason is a decrease in the share of preferential mortgages in loans. Currently, 45% of new housing loans are being issued at market rates, which is the maximum over the past two years. Their rates average 17-18% per annum.

At a high rate, extending the mortgage term does not significantly reduce the monthly payment, but greatly increases the total amount of payments to the bank. So, the overpayment on a 30-year loan for an apartment for 17 million with a down payment of 30% will amount to about 52 million rubles, which is three times higher than the price of the property itself. However, if you reduce the term to 25 years, the overpayment will be reduced by 10 million, and the monthly payment will increase by only 1,000 rubles. And if you reduce it to 15 years, the overpayment will decrease immediately to 32 million, while the monthly payment will increase by only 7%.

The banks' data confirms the changes in the market. VTB's average mortgage term decreased from 27.4 years in January to 24.3 years in June, its press service told Izvestia. This is attributed to an increase in the market share of mortgages, which is expected to exceed half of all loans in the second half of the year.

A similar trend is seen in Sberbank's Domclick service: borrowers still take out loans for a maximum of 30 years under preferential programs, while market mortgages usually take out terms of about 10-12 years.

The demand for preferential programs decreased after the change in the terms of the family mortgage, said Vasily Kutyin, Director of Analytics at Ingo Bank. The "one preferential loan per family" rule has been in effect since February 1. Many borrowers rushed to apply for a mortgage before the new requirements came into force, so after their introduction, demand temporarily decreased.

How profitable is it to shorten the mortgage term?

The main advantage of a short loan is saving on interest. Those who can afford a higher payment are increasingly choosing a shorter term, said Liana Kadyrova, an expert at Compare. With a stable income, this allows you to pay off the debt faster and greatly reduce overpayments.

However, the savings come at a cost of increasing monthly expenses. If the family's income drops due to job loss, illness, or other reasons, it will become much more difficult to service such a loan. In addition, if the deadline is short, the bank may approve a smaller amount or require a larger down payment, Vasily Kutyin warned.

Therefore, many experts recommend a different strategy: apply for a long-term mortgage in order to reduce the mandatory payment, and then, if there is free money, close the loan ahead of schedule with a shorter term. This approach gives more flexibility, said Vadim Butin, head of the mortgage lending department at Glavstroy-Real Estate.

A long term does not mean that you will have to pay for decades — if you wish, you can always close the loan earlier, confirmed Natalia Milchakova, a leading analyst at Freedom Global. But in case of temporary difficulties, a small mandatory payment reduces the risk of delays.

What should a borrower do with such rates?

When the mortgage term is shortened, the final overpayment does noticeably decrease, and the higher the rate, the stronger this effect, said Andrey Girinsky, associate professor at the Faculty of Economics at RUDN University. In the case of housing loans at the market rate, it makes sense to shorten the term as quickly as possible. However, it is often more profitable to pay off a low-interest mortgage on schedule, concluded Yulia Kovalenko, an economist at Plekhanov Russian University of Economics.

At the same time, you can put extra money on a deposit, the interest on them is twice as high as the rate on a preferential mortgage. If the deposit is replenished regularly, at the end of the term it will accumulate an amount exceeding the total overpayment.

It is also important to consider how the borrower's income will change. Over time, the same monthly payment amount may become less noticeable. For example, with a salary of 100 thousand rubles, a payment of 50 thousand is half of earnings, and with an income of 150 thousand, it is already about a third.

However, if earnings do not increase, even a fixed payment becomes more burdensome over time, Vasily Kutyin warned. In this case, due to inflation, an increasing part of earnings will be spent on daily expenses.

The main question for those who do not have access to preferential programs is: should I take out a housing loan now or wait? Market mortgages are becoming massively justified at rates of about 10% per annum — this level is possible when the key value drops to a neutral value of 7.5–8.5%, explained Igor Rastorguev, a leading analyst at AMarkets. Now, at rates of 17-23% per annum, a loan without government support remains unprofitable for most Russians: the loan payment is several times higher than the rent for similar housing, he added.

For example, when buying a two—room apartment for 15 million rubles with a down payment of 35% for 20 years, the payment on a preferential mortgage (6%) will amount to about 70 thousand rubles, at a market rate of more than 160 thousand, the financial adviser and founder of Rodin estimated.Capital Alexey Rodin. At the same time, the rent of similar housing in the capital region, according to Avito Real Estate, is about 73 thousand rubles per month.

Therefore, for a family without benefits, a reasonable strategy today is to rent a house and at the same time save the initial payment on deposits, Igor Rastorguev believes. Now the rates on them are on average 13% per annum, follows from the data of Finuslug.

Also, a market mortgage can be considered with an extremely high down payment — from 50% and above, Igor Rastorguev specified. In this case, the loan amount and overpayment become significantly less, but this option is not available to everyone.

However, there is no universal recipe — everything depends on the stability of income and life plans, experts agree. It is better to apply for a loan with a more convenient payment and, if possible, repay it ahead of schedule. In an environment where the stakes can change at any moment, this approach leaves room for maneuver.

Переведено сервисом «Яндекс Переводчик»