The burden is longing: Russians' overdue loans have reached a record 1.6 trillion

Citizens' overdue loans have reached a maximum of 1.6 trillion rubles — last year it increased by almost a third, according to data from the Central Bank, which was studied by Izvestia. At the same time, the share of problem consumer loans jumped to 4.6%, which is more than four times higher than for mortgages. The delay has been accumulating throughout the year, despite the Central Bank's attempts to limit risky lending. Already, this affects the behavior of banks — only one out of five borrowers can get a loan. What level of "bad" debts will create risks for the economy is in the Izvestia article.

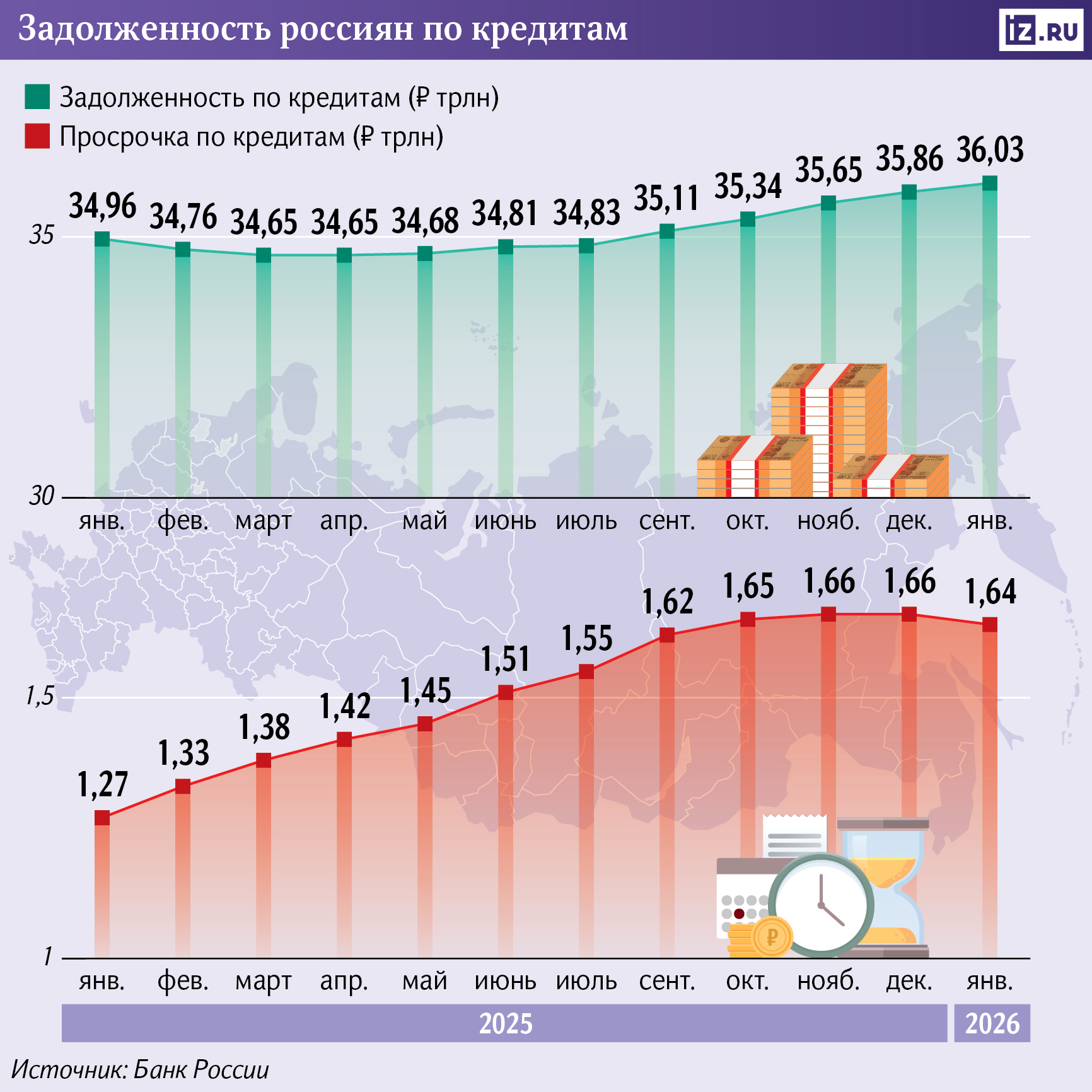

How much has the level of "bad" debts increased?

By the beginning of 2026, the volume of overdue loans on unsecured loans to the population reached a record 1.65 trillion rubles. This is almost a third more than a year earlier, according to data from the Central Bank, which was analyzed by Izvestia.

At the same time, the share of "bad" debts rose to 4.6%, which was the highest in the last five years. The indicator was at a higher level only in March 2021, according to the regulator. This is more than four times the share of mortgage delinquency, where it remains below 1%. Nevertheless, even in this segment, the situation has worsened — over the year, the volume of overdue housing loans has more than doubled and exceeded 200 billion rubles.

The main reason for the increase was the "maturation" of unsecured loans issued during the active credit boom, said Dmitry Gritskevich, Head of Banking and Financial Market Analysis at PSB. According to him, in 2023-2024, banks rapidly increased their portfolio, including through borrowers without a credit history, the risks of which were difficult to accurately assess.

"Loans in 2024 really show an increase in delinquencies as they mature," confirmed Alexey Volkov, Marketing Director of the National Bureau of Credit Histories (NBKI).

During the life of the loan, the risk of its going into arrears increases due to changes in solvency. The situation could also be affected by inflation — according to the Central Bank, back in early 2025 it exceeded 10% and only by the end of the year it amounted to 6.6%.

At the same time, the current levels of delinquency do not reach historical highs, said Ivan Uklein, Senior Director for Bank Ratings at Expert RA agency. According to him, in 2015 the share of problem loans exceeded 8%, whereas now it is noticeably lower. In addition, banks have formed significant reserves in advance for possible losses, which reduces risks for the sector.

The peak growth in retail loan delinquencies has already passed, Alexey Volkov noted. According to him, it occurred in the third quarter of last year. The situation for new loans issued in 2025 looks more stable, and delinquencies in the early stages of life of such loans have noticeably decreased. This is due to the tightening of Central Bank regulation and a decrease in banks' risk appetite.

By mid-2025, half of the debt owed by individuals was still owed to borrowers with three or more loans, said Anna Zemlyanova, chief analyst at Sovcombank. Now their share is gradually decreasing, including due to restrictions on granting loans to customers with high debt loads.

The Central Bank does not prohibit such loans completely, but strictly regulates their share. For example, in car loans, banks have the right to issue no more than 5% of new loans to customers who spend 80% of their income on paying off their debts. This reduces risks for financial institutions and protects customers from credit overload.

The quality of the new issues has improved significantly, Dmitry Gritskevich emphasized. According to the Central Bank, at the end of 2023, the share of consumer loans with increased risk was 40%, at the end of 2024 it decreased to 27%, and in the third quarter of 2025 — to 19%. This reduces potential risks over the horizon of 2026-2027, although the effect of stricter regulations is gradually manifesting itself.

At the same time, the growth of "bad" loans remains noticeable due to a slowdown in disbursements, the VTB press service noted. The Central Bank's regulation restrains the volume and pace of lending, which is why the portfolio does not grow so quickly, and the accumulated arrears remain in the statistics longer.

Izvestia sent a request to the Central Bank about the consequences of an increase in the level of overdue debt.

Why banks are approving loans less and less often

The growth of problem debts in the market as a whole leads to stricter regulatory measures, the press service of Novik Bank explained. This directly affects the approach of banks to new loans and the assessment of borrowers.

The increased delay has a particularly strong effect on consumer credit disbursements, Dmitry Gritskevich noted. Banks are putting increased risks into interest rates and risk policies, which is why there are fewer approvals and the cost of loans is decreasing more slowly than the key rate.

By the end of 2025, the share of retail loan approvals dropped to a minimum of 17-18%, according to NBKI data. In fact, consumer loans are now issued less frequently than in one out of five cases.

The share of overdue loans at 4.6% does not look critical, but its growth rate is alarming — almost a third in a year, said Natalia Milchakova, a leading analyst at Freedom Finance Global. According to her, this indicates a decrease in the solvency of certain groups of the population.

The increase in delays reflects the general deterioration of the financial situation of citizens, says Igor Dodonov, an analyst at Finam Financial Group. According to him, the situation is affected by inflation, the difficult economic situation and the growing debt burden of the population.

Salaries in Russia have been growing at a record pace, but in fact they have not increased for everyone, said Natalia Milchakova, a leading analyst. According to the Sbera survey, 55% of Russians saw an increase in income in 2025, 34% saw a decrease, and 11% did not change.

This is due to the deterioration of the financial condition of the business, the expert added. Many companies were forced to either cut staff or reduce salaries due to the slowdown in economic growth amid the still high key interest rate, even though it was reduced from 21% to 16%.

In the near future, the increase in delays may continue, says Igor Dodonov, an analyst at Finam Financial Group. Banks, he said, will maintain a strict issuance policy, while the approval rate will remain low. To reverse the trend, an improvement in the economic situation and an increase in real incomes of citizens are necessary, but it is difficult to count on this in 2026.

Improvement of the delay situation is possible in the second half of the year, admits Natalia Milchakova. According to her, lower interest rates and a gradual recovery in the economy may lead to a decrease in the share of overdue loans to 3.5–4% by the end of 2026.

Переведено сервисом «Яндекс Переводчик»