Disbelief Loan: Banks turn around eight out of ten borrowers

Obtaining a loan has become an extremely difficult task for most Russians — banks have almost stopped approving them: at the end of 2025, up to 83% of loan applications were rejected. The reason is not only the caution of creditors, but also the harsh policy of the regulator and the growing risks in the economy. Why loans remain practically unavailable, despite the reduction in the key rate, what conditions are important to comply with in order to obtain a loan and when it will become easier to apply for it — in the Izvestia article.

What are the chances of getting a loan approved in 2026?

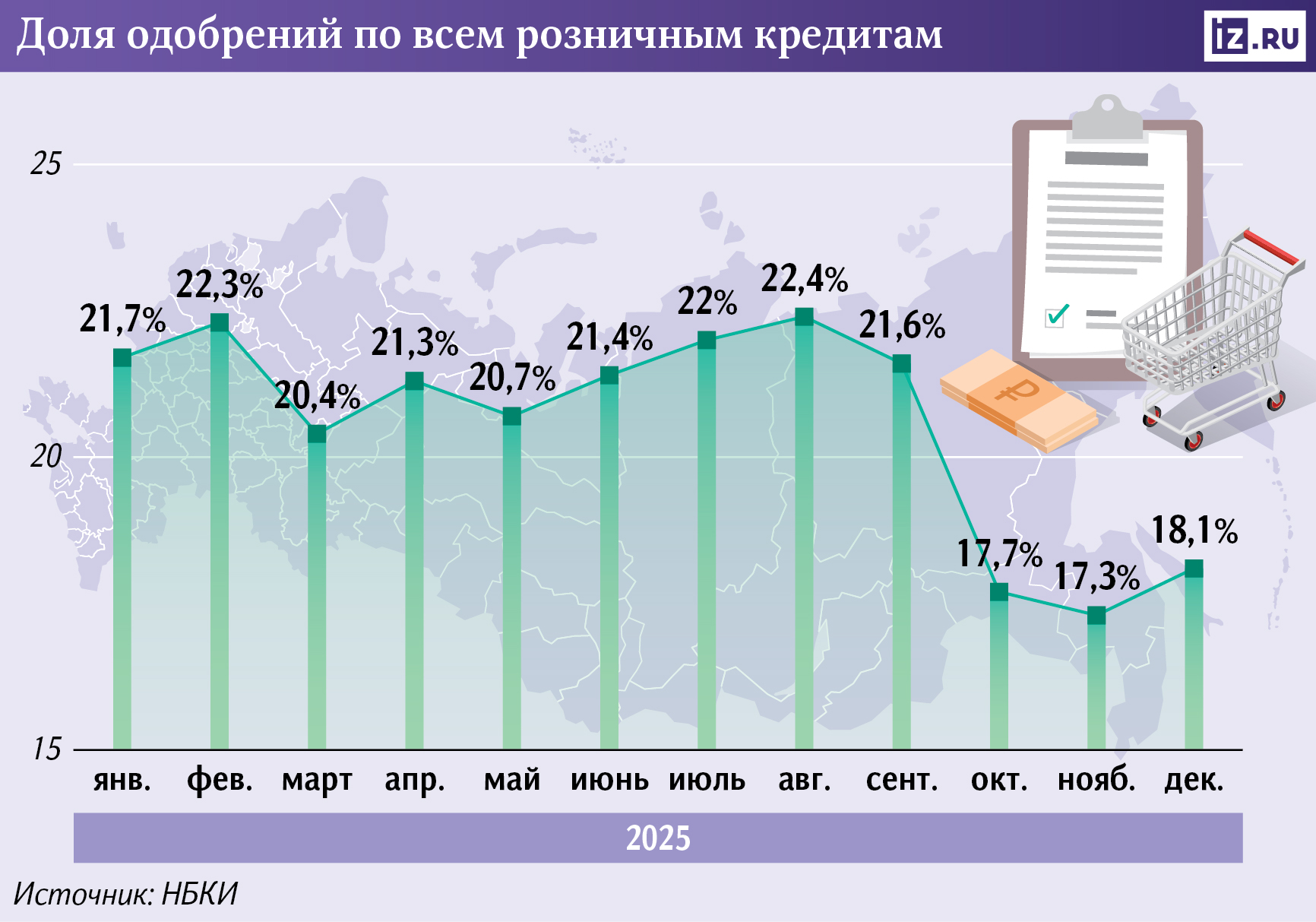

The share of retail loan approvals dropped to a minimum of 17-18% by the end of 2025, according to data from the National Bureau of Credit Histories (NBCI), which was studied by Izvestia. This means that banks are now rejecting more than 80% of applications. A sharp increase in refusals occurred precisely in the fourth quarter of 2025, with the average approval rate of about 22.6% over the same period last year.

Car loans were the most difficult category, with a failure rate of up to 84%. Consumer loans are granted less often than in one out of four cases. The mortgage situation is slightly better: by the end of 2025, banks approved about 35% of applications. At the same time, the figure exceeded 50% in the summer.

Banks deliberately keep their disbursements low and are not ready to quickly increase risks, since the quality of their portfolio is more important to them now than the volume of loans, explained Alexey Volkov, NBKI Marketing Director.

Izvestia sent a request to the Central Bank about the reasons for the decrease in the share of loan approvals.

Macroprudential limits (MPL) play a central role in this process, they limit the issuance of loans to borrowers with a high debt burden. The Central Bank does not prohibit such loans completely, but strictly regulates their share. For example, in car loans, banks have the right to issue no more than 5% of new loans to customers who spend 80% of their income on paying off their debts. This reduces risks for financial institutions and protects customers from credit overload.

The decrease in the share of approvals against the background of such restrictions suggests that the demand for borrowed money from already lent Russians remains high, even despite stricter regulations.

The main reason for the increase in consumer loan refusals is precisely the Central Bank's measures to combat risky loans, said Dmitry Gritskevich, Head of Banking and Financial Market Analysis at PSB. According to the regulator, in the third quarter of 2025, the share of such loans decreased to 19% against 29% a year earlier.

Even with credit cards, banks primarily look at the debt burden: if 80% of income or more is spent on payments, they will refuse a new loan, he explained.

Additional pressure is created by an increase in delinquency: the share of problem loans in banks' portfolios reached 12.9% as of October 1, 2025, against 7.9% a year earlier, Dmitry Gritskevich added. This logically leads to stricter requirements for potential borrowers, said Natalia Milchakova, a leading analyst at Freedom Finance Global.

The statistics could also be partially influenced by the seasonal factor: by the end of the year, demand for loans is traditionally growing, said Ivan Uklein, Senior Director of Banking Ratings at Expert RA. For example, according to Frank RG, in December, the issuance of family mortgages exceeded 800 billion rubles, which is one and a half times more than a month earlier.

Why do banks have a hard time giving loans to Russians

The key rate has been decreasing since the summer of 2025 — it dropped from 21% to 16%, but this factor affects the level of loan approvals with a delay, explained financial expert Fyodor Sidorov. Banks fear an increase in delinquency, the economy has not yet fully recovered from overheating, and inflation expectations remain high — in December, Russians expected price increases to accelerate next year to 13.7%, although annual inflation dropped to 5.6% by the end of 2025.

Even against the background of a reduction in the interest rate, banks continue to introduce uncertainty into their policies — the instability of household incomes, the growing debt burden and regulatory pressure, said Magomed Gamzaev, Director of financial product development at the financial marketplace "Compare". According to him, the market is now choosing caution rather than aggressive growth.

Reducing the key rate and stabilizing loan rates is not enough yet to bring borrowers with a good credit history back to the market, who prefer to save rather than take on debts, said Alexey Volkov from NBKI.

Car loans remain a separate problem — their availability has sharply decreased due to the growth of recycling, Fyodor Sidorov noted. In 2025, it increased 1.5–2 times — for new passenger cars, the fee increased to an average of 300-600 thousand rubles, which directly accelerated prices and increased the number of refusals.

The low number of car loan approvals is also related to new income verification requirements, added Natalia Milchakova from Freedom Finance Global. Banks now issue such loans only after an official check through Gosuslugi or a Social Fund, so it has become almost impossible for borrowers with gray salaries to get a loan. Rising car prices have also increased the amount of loans, and banks are only willing to give large loans to a limited number of customers.

Mortgages remain an exception, as they are secured loans with collateral in the form of apartments and active government support, Magomed Gamzaev noted. However, even here, banks are more likely to reject borrowers with down payments below 30%, sifting out many at an early stage.

A decrease in the number of approvals makes large purchases and housing less affordable for future borrowers, Natalia Milchakova emphasized. According to her, many Russians will have to postpone plans to improve their living conditions indefinitely.

How to get loan approval in 2026

Quick and formal approvals are becoming a thing of the past — banks are analyzing their credit history, debt burden and income stability more and more deeply, noted Magomed Gamzaev from Compare.

"When considering an application, the officially confirmed income is mainly taken into account, which makes it difficult to obtain loans for a number of categories of citizens, including the self—employed," the press service of Novik Bank explained.

Borrowers with a high credit rating — above 750 points — now have an approval rate of 43%, which is significantly higher than the average level, said Alexey Volkov from NBKI. He advises you to closely monitor your credit history and prevent it from deteriorating.

To increase the chances of approval of the application, it is also important to reduce the debt burden, repay part of the loans or officially confirm income growth, as well as request a smaller loan amount, explained Dmitry Gritskevich from PSB. If there are unused credit cards, they should be closed — when assessing the amount of customer debts, banks look at the entire plastic limit approved, Novik Bank added.

An increase in the share of approvals is possible in the second half of 2026 against the background of a decrease in the level of overdue loans on the balance sheet of banks and cheaper loans after reducing the key one, Dmitry Gritskevich believes. Easing the Central Bank's policy may reduce monthly payments and make loans more affordable.

A steady increase in approvals is possible only with a decrease in inflation, a recovery in incomes and a relaxation of regulatory requirements, Magomed Gamzaev emphasized. Banks will return to active lending only after they are confident in the stability of the economy. We can expect a noticeable improvement in the approval situation if the interest rate is lowered below 12-14% and inflation is controlled, concluded Fyodor Sidorov.

Переведено сервисом «Яндекс Переводчик»