- Статьи

- Economy

- Unfavorable weather: Russia intends to reduce the share of government programs in mortgage loans to 30%

Unfavorable weather: Russia intends to reduce the share of government programs in mortgage loans to 30%

The Ministry of Finance intends to reduce the share of government programs in mortgages to 25-30%, Deputy Finance Minister Ivan Chebeskov told Izvestia. The agency expects that this level will be achieved by 2030. At the beginning of the year, the share of preferential mortgages in mortgage loans for new buildings reached about 90%. However, the authorities do not want to base their state policy on massive support for the housing market. If the benefits are no longer targeted, it reduces the availability of real estate for Russians. By July, the authorities will announce new conditions for the family mortgage. How the market will change as the key one decreases and why there will be no sharp decrease in the share of government programs — in the Izvestia article.

To what level can the share of government programs in mortgage loans fall

The vast majority of loans for new housing in Russia today are issued on preferential terms, Deputy Finance Minister Ivan Chebeskov told Izvestia. According to him, the share of government programs in mortgage loans in the primary market at the beginning of the year was about 90%. However, the Agency would like to see a higher level of housing loans on market terms, as excessive dependence on subsidies distorts the structure of the market.

"It is wrong to base government policy on the fact that most of the lending will be carried out on preferential terms,— stressed Ivan Chebeskov.

The share of government programs should eventually drop to the target level of 25-30%, the Deputy Finance minister noted. The press service of the department added that the indicator could drop to this level by 2030.

When asked by Izvestia about the new conditions for family mortgages and their impact on the share of government programs in disbursements, the deputy minister clarified that no drastic steps were planned to achieve the target level. The reduction in the share of preferential mortgages will occur gradually. This includes a decrease in the key interest rate and an increase in market loans.

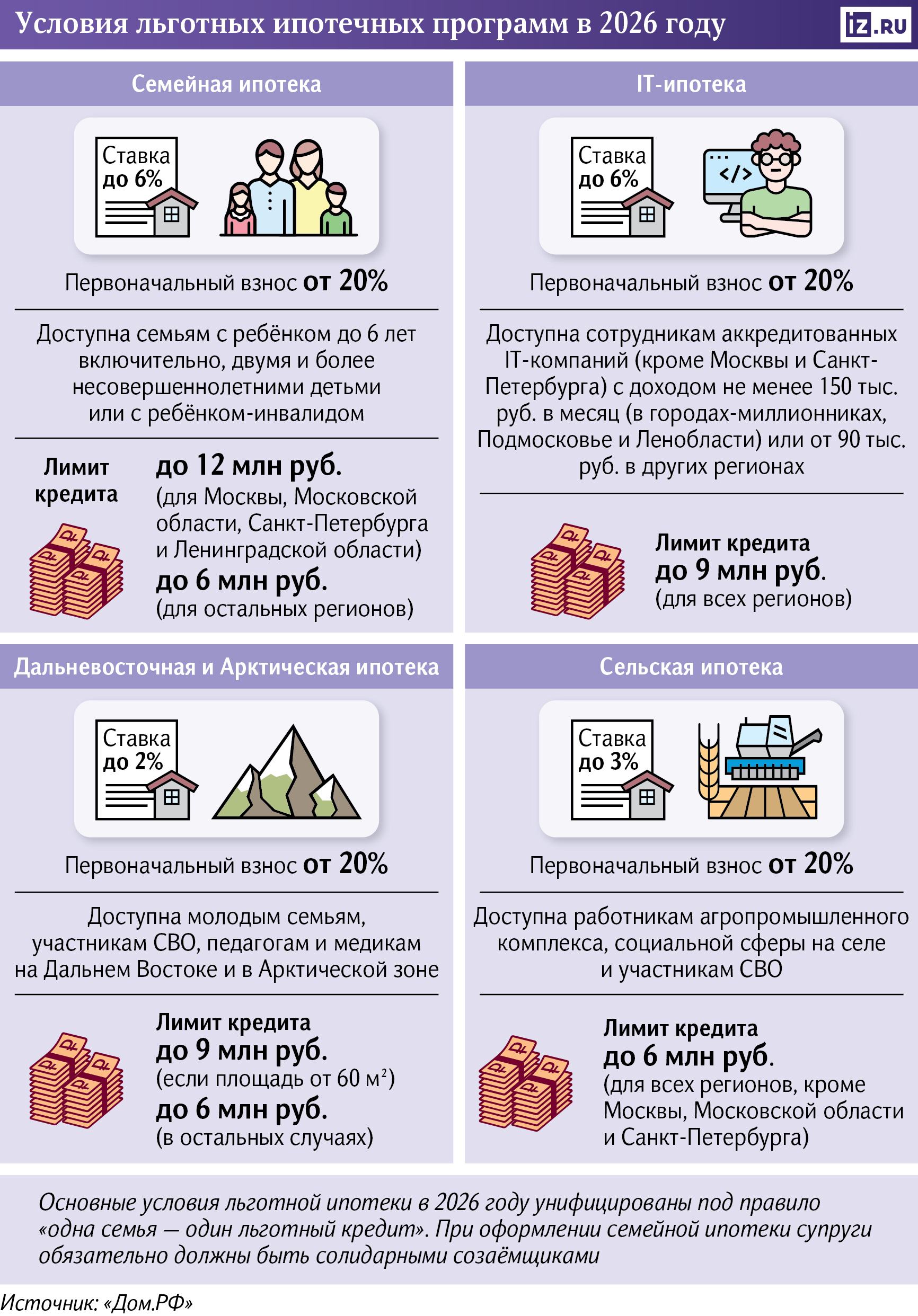

The government instructed the Ministry of Finance and the Ministry of Construction to work out the idea of a differentiated family mortgage rate by July 1, 2026. According to this concept, the rate may depend on the number of children: for families with one child, the level of 10-12% is discussed, with two — about 6%, with three or more — about 4%. The possibility of automatically changing the rate at the birth of a child is also being considered in order to simplify the procedure for borrowers and reduce the administrative burden.

However, no final decisions have been made yet. According to Ivan Chebeskov, the program parameters will be determined separately, and the government will submit the official terms by July 1.

What is the share of government programs in mortgage loans

Today, the share of government programs in the total volume of mortgage loans is lower than in the primary market. According to Dom.Russia", in May, Russians issued housing loans worth 332 billion rubles, of which about 55% accounted for preferential programs. The main contribution to this indicator is provided by the family mortgage, which indicates the high dependence of the segment of new buildings on government support.

At the same time, the market segment is gradually recovering. Savings Bank records a 3.3-fold increase in mortgage loans under such conditions compared to last year, while about 60% of such loans are for ready-made housing.

New buildings remain the most dependent segment on preferential programs, which is confirmed by data from other market participants. In Bank Saint Petersburg, the share of government programs for the purchase of new buildings on credit reaches 67%, while the average for the portfolio is lower. But in some banks, the share is still high — for example, in VTB, by the end of May, it reached 83%, the organization's press service said.

Why does the Ministry of Finance want to reduce the share of government programs in mortgage loans

Subsidizing rates creates a significant burden on the budget, said Natalia Bogomolova, director of NRA Ratings of financial institutions. This is due to the fact that the government compensates banks for the difference between preferential and market rates, which is significant in the current conditions.

The amount of compensation is calculated according to the formula "key rate + 3.5%", which is now equivalent to about 18%. At the same time, the borrower pays about 6%, and the remaining part is actually subsidized by the state. As a result, the budget takes on two thirds of the interest burden on most housing loans issued.

The average mortgage term already exceeds 26 years, according to data from Frank RG. This means that the government has been obligated to compensate for the difference in rates for decades, and new loans are constantly increasing the total amount of future obligations.

In 2025, the cost of preferential mortgage programs reached about 2 trillion rubles, which was a historic high, Natalia Bogomolova added. In 2026-2028, about 1.8 trillion rubles were mortgaged on family mortgages alone, said Valery Tumin from FAM Properties. At the same time, the actual expenses are already exceeding the planned targets.

— A high proportion of preferential mortgages is a signal that the housing market depends on the state. If 90% of disbursements come from government programs, it means that without subsidies, the dominant part of buyers simply cannot take out a loan," said Evgenia Veselova, an expert at the financial marketplace Compare.

Preferential mortgages support demand and thus help prices rise, added Vladimir Chernov, analyst at Freedom Finance Global. The buyer looks primarily at the monthly payment, and not at the full cost of the apartment. Developers take this into account, and part of the benefit from the low rate goes into the price per square meter.

As a result, against the background of massive preferential mortgages for new housing from 2020 to 2024, new buildings rose in price by about 1.7 times, and the gap between the primary and secondary markets reached historic highs, concluded Valery Tumin. According to the latest data, it exceeded 90% in Central Russia.

All this creates a systemic risk: if the parameters of state support change, the market may react sharply by reducing demand and adjusting prices, the expert added.

The market may experience a similar shock in the second half of 2026 against the background of adjusting the conditions of the family mortgage, on which people and developers largely depend. Against the background of the changes, about 2.7 million families with one child may lose the opportunity to apply for a loan at a rate of 6% per annum and will be forced to take out a mortgage at a higher interest rate, Izvestia wrote earlier.

When will the share of government programs in disbursements be able to decrease

"Changes in the terms of family mortgages may help reduce the share of government programs in total disbursements if the updated terms are more targeted (aimed at supporting large families) and limit the use of the program for investment purposes," said Olga Kovalenko, head of the Mortgage Lending Department at Sovcombank.

However, the key factor remains the reduction of the key interest rate and the convergence of market conditions and preferential programs, experts interviewed by Izvestia emphasized.

But even with the easing of monetary policy, a sharp restructuring of the market should not be expected, Ekaterina Samyshina said. The key rate may decrease to 12-13% by the end of the year, which will support the growth of market disbursements, but will not make them more profitable than preferential programs.

More noticeable changes are possible with a further reduction in the rate. At the current level of about 14.5%, market rates are in the range of 17-18%, which makes them inaccessible to most borrowers, Valery Tumin emphasized. This gap makes preferential programs more profitable for many borrowers.

With a key rate of about 8%, loans in the range of 10-12% may appear on the market, which will partially increase competition with preferential mortgages, primarily in the secondary housing segment, explained Tatiana Reshetnikova from the Floors company. By this point, the upper level of family mortgage rates will be approximately at the same level, which will equalize conditions for many borrowers.

Reducing the share of government programs to 25-30% is possible only in the long term and with a steady reduction in the cost of loans, concluded Freedom Global analyst Vladimir Chernov. It will take at least two to three years. However, even in this scenario, the market will remain significantly dependent on budget support.

Переведено сервисом «Яндекс Переводчик»