Deposit settlement: Russians have become more likely to open deposits after interest rates decrease

- Статьи

- Economy

- Deposit settlement: Russians have become more likely to open deposits after interest rates decrease

In April, the number of new deposits increased by 27% compared to last year, according to an analysis of the Finuslugi marketplace, reviewed by Izvestia. Russians have become more active in opening deposits, despite the fact that profitability has fallen by 6 percentage points during this time. At the same time, most often people invest only for up to six months — citizens prefer to maintain liquidity even at the expense of potentially higher returns. How it is more profitable to invest money now is in the Izvestia article.

Why Russians are more active in opening deposits

Russians began to open deposits at an accelerated pace. In April, the number of new deposits increased by 26.8% compared to the same month last year, according to analysts at the Finuslugi marketplace. At the same time, the average rate decreased significantly — in April 2026 it was slightly less than 15% compared to 21% a year earlier. During this time, citizens also began to place larger amounts — the so-called average check increased by 8%, to 462.7 thousand rubles.

This is a rational reaction to market expectations, explained Maria Ermilova, International Financial Advisor, Candidate of Economics, Associate Professor of Finance for Sustainable Development at Plekhanov Russian University of Economics. When rates begin to decline, depositors tend to lock in returns while they remain relatively high.

The trend is directly related to the dynamics of the key rate, said Denis Astafyev, fund manager and founder of the SharesPro fintech platform. During the year, the Central Bank lowered it from 21 to 14.5%, the expert recalled.

Russians see a steady downward trend in rates, Igor Rastorguev, a leading analyst at AMarkets, agreed. Moreover, this trend will continue.

Why do people choose short deposits?

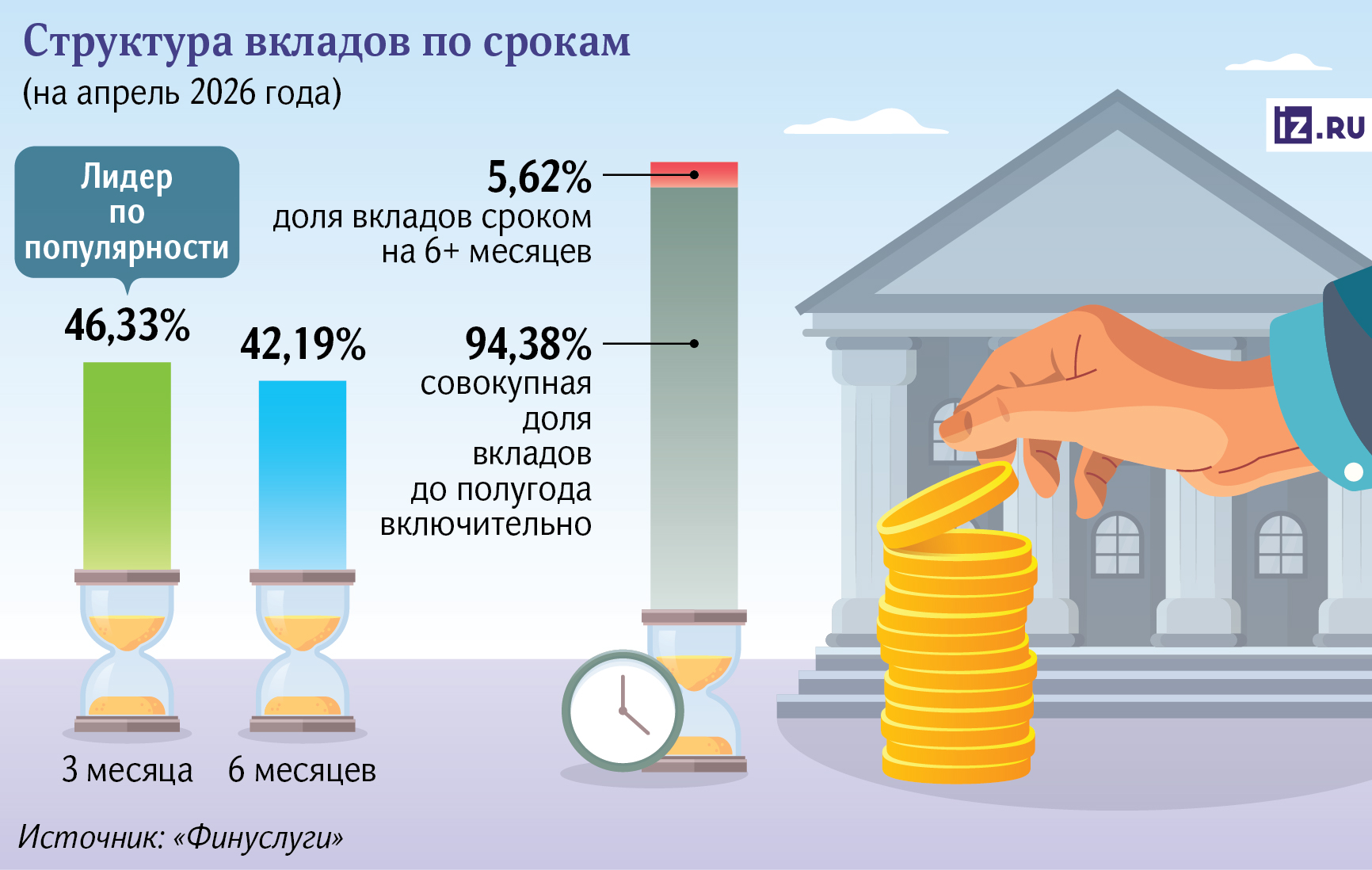

In April, Russians opened almost all new deposits for short periods of up to six months. The share of such deposits was 94%, it follows from the data of Finuslug. Three—month deposits are among the leaders (46%), while the share of semi-annual deposits increased by almost 13 percentage points over the year, to 42%.

The reasons are distrust of long—term forecasts and the need for liquidity, Maria Ermilova believes. In conditions of economic uncertainty, Russians prefer to remain flexible: short deposits allow them to quickly access funds or transfer them to more profitable instruments.

Citizens strive to preserve the possibility of an operational redistribution of funds — this is a classic strategy of behavior in a falling interest rate market, Igor Rastorguev agreed. Banks, in turn, benefit from attracting short-term resources more cheaply and issuing longer loans more expensively, capitalizing on the time difference.

In fact, depositors adhere to a strategy of regularly shifting capital in anticipation of better conditions, Denis Astafyev noted.

The predominance of short deposits is also related to expectations of a further reduction in the key interest rate, said Evgeny Romanov, a leading analyst at Expert RA. Terms of up to six months ensure a balance between profitability and liquidity, and also preserve the opportunity for the depositor to quickly change the strategy. The Director of Financial Product Development agreed with this. "Compare.<url>" Magomed Gamzaev.

The psychology of depositors also plays a role: in conditions of turbulence, the population increasingly considers deposits not as a tool for increasing capital, but as a "safe haven" to protect savings from inflation, added financial adviser and founder Rodin.Capital Alexey Rodin. In addition, people prefer to remain cautious: about 68% of Russians, according to the analyst, are concerned about their financial future. In such circumstances, short deposits are perceived as a safer solution, he believes.

Long-term deposits are more profitable

Despite the popularity of short deposits, in terms of net profitability, long deposits remain more profitable in many cases, experts say. When fixing the rate for a long time, a person protects himself from further reduction, explained Maria Ermilova. If the key continues to fall, then each new short deposit will be issued at a lower percentage, which will reduce the final profit.

Currently, the average yield of the top 10 banks on deposits up to 90 days is 13%, and on annual deposits - 12.68%, Igor Rastorguev noted. According to his calculations, placing 1 million rubles on an annual deposit at such a percentage can bring about 126.8 thousand rubles of income. If funds are consistently placed on short deposits with a gradual reduction in rates, for example, up to 10%, the final profit will be about 82.5 thousand rubles. Thus, long-term fixation can provide an advantage of more than 40 thousand rubles.

The strategy of constantly "shifting" funds is psychologically comfortable, but mathematically inferior to long-term deposits, Denis Astafyev emphasized.

Long-term deposits lose in profitability more slowly. As the head of the expert analytics department "Banks.<url>" Inna Soldatenkova, the maximum interest rates on short-term deposits have dropped by 7-7.5 percentage points over the year. At the same time, the yield on two-year deposits has decreased by 5.8 percentage points. The market is gradually leveling off the yield curve over time, and this trend is likely to intensify, the analyst believes.

What are the risks of short deposits?

The main risk of investing in the short-term model is that the market may continue to move towards lower rates, said Evgeny Romanov, a leading analyst at Expert RA.

In addition, short deposits increase the dependence of the population's decisions on the news background and market expectations, Alexey Rodin added. According to him, now people are increasingly managing liquidity rather than forming long-term savings.

At the same time, participants in the financial system do not consider the current deposit structure to be a threat to the stability of the banking sector. The Deposit Insurance Agency noted that the volume of the fund and the number of insured events do not depend on the timing of the placement of funds and remain stable.

The Bank of Russia takes a similar position: the predominance of short deposits does not create liquidity risks, since in most cases the population does not withdraw money from banks, but reissues them for new deposits, the press service of the Central Bank told Izvestia. At the same time, the regulator is working to stimulate long-term savings: initiatives have already been introduced to differentiate insurance premiums in the Federal Reserve Fund and increase insurance coverage for long-term deposits.

The Compulsory Deposit Insurance Fund is a special fund from which compensation is paid to depositors of banks in the event of license revocation or bankruptcy of a credit institution. The Fund is formed by regular contributions from banks — participants in the deposit insurance system are required to transfer them. The fund is managed by the Deposit Insurance Agency (DIA).

The growing popularity of deposits reflects the population's adaptation to the new interest rate cycle, experts agree. Russians are striving to lock in the remaining high returns, while maintaining flexibility in the face of uncertainty. Depositors are balancing between maximum profit and the ability to respond promptly to changes in the economic situation.

Переведено сервисом «Яндекс Переводчик»