One bottom: bad debts of Russians jumped by a third

The bad debts of Russians exceeded 2.4 trillion rubles by the end of 2025. They have jumped by a third in a year, according to data from the Bank of Russia, which was studied by Izvestia. We are talking about loans that have already defaulted — the growth of such debts is primarily due to high interest rates and a slow increase in household incomes. It becomes more difficult for borrowers to service expensive loans, especially if they have multiple obligations. But until the problem debts are written off, banks are required to keep them on the balance sheet and form reserves for them. Because of this, they are more cautious in approving new loans and slower in lowering rates.

Why has the share of problem loans increased?

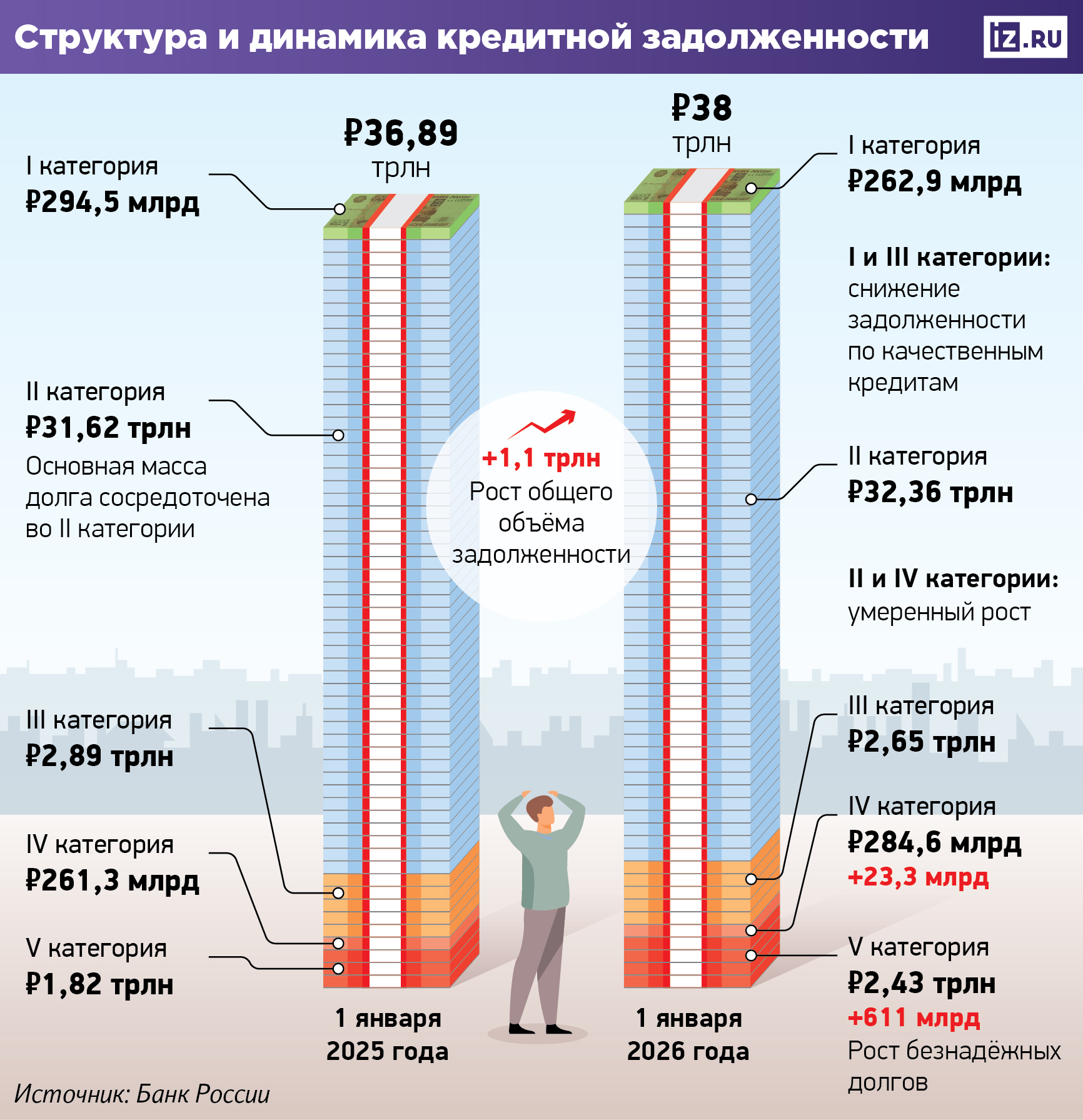

Russians' debt on loans of the lowest quality exceeded 2.4 trillion rubles last year, according to statistics from the Bank of Russia. In 2024, there were a third fewer of them — about 1.8 trillion. Such loans can be considered non-refundable, they belong to the fifth category of quality.

Problem debt is formed due to loans of the fourth and fifth categories. Collectively, they account for almost 7% of banks' retail loan portfolio, according to the Central Bank. A year ago, their share was about 5.7%.

In fact, every 14th ruble in the retail portfolio of banks is associated with a serious risk of non-repayment. These are no longer just risky loans, but loans for which financial institutions initially expect significant or almost complete losses, said Ilya Fedorin, Associate Director for Ratings of credit institutions at Expert RA.

In the Russian risk assessment system, loans are divided into five quality categories. Category I loans are considered the most reliable and have minimal risk. Category II assumes moderate risk and requires the formation of a reserve of up to 20% of the debt amount. Category III — doubtful loans with a reserve of 21 to 50%. Category IV is considered problematic: the probability of non-repayment is high, so banks form a reserve at the level of 51-100%. Category V — bad loans. According to them, the probability of losses is estimated at 100%, so banks are required to reserve the entire amount.

In the segment of unsecured consumer loans, the share of problem loans increased to 13% at the beginning of 2026 against 9% a year earlier, the regulator's press service explained to Izvestia. Payment discipline for debts issued in late 2023 and early 2024 has mostly deteriorated. Among them are loans from borrowers with low credit ratings or no credit history at all, which initially made it difficult to assess the risks.

The mortgage situation remains more stable. The share of problem loans has increased, but remains at a low level — about 1.7% at the beginning of 2026, the Central Bank said. This is due to the "maturation" of loans that banks issued during the period of high demand for preferential mortgages and market programs in 2023-2024.

The increase in problem debts is also associated with a slowdown in household income growth, said Vladimir Chernov, analyst at Freedom Finance Global. During the time after the loans were issued, borrowers' expenses could increase due to inflation. If incomes did not increase, it would become much more difficult for them to service the loan.

The situation is particularly difficult for borrowers who have several loans at once, the press service of the National Association of Professional Collection Agencies (NAPCA) reported. The more revenue is allocated to pay creditors, the more likely such a client is to default over time. Each additional debt increases the risk of bankruptcy by about 20-25% at the average household income level.

At the same time, banks form significant reserves for problem loans in advance. According to the Central Bank, the total amount of such an airbag for loans of the fourth and fifth categories is about 2.3 trillion rubles. This is significantly more than a year earlier — 1.8 trillion.

How will the growth of problem debt affect the economy

The growth of problem loans is also reflected in the statistics of personal bankruptcies. In 2025, almost 568 thousand citizens were declared insolvent, which is 31.5% more than a year earlier, said Fyodor Sidorov, founder of the School of Practical Investment. This is a record for the entire existence of the institute of personal bankruptcy in Russia. Moreover, in 97% of cases, citizens themselves initiate the procedure.

However, in practice, we are often talking about the influence of law firms, which often impose debt cancellation services, the expert added. The market works aggressively — such "helpers" often find people who are over-indebted themselves and offer them a quick bankruptcy, effectively leading them away from negotiations with the bank. As a result, some borrowers begin the procedure even before the loan officially becomes problematic.

In fact, such companies do not create debt problems, but accelerate the conversion of debts into defaults, Fyodor Sidorov noted. As a result, the statistics of problem loans look worse than they could have been without their participation.

The growth of problem debts is an early signal of a deterioration in the financial situation of households, Vladimir Chernov noted. When the share of such loans increases, it means that some borrowers can no longer cope with the debt burden. This leads to a slowdown in consumer demand, resulting in lower spending on goods and services.

The increase in the cost of loans and day-to-day expenses causes chronic delinquencies: loans move into more risky categories, and banks increase reserves, said Ilya Fedorin from Expert RA. As a result, the cost of risk is rising, financial institutions are more cautious about issuing new loans, tightening requirements for borrowers, and lowering rates more slowly.

Loans of the fourth and fifth categories are loans for which banks no longer expect to repay the money in full, Fyodor Sidorov recalled. Reserves for such loans actually freeze part of their funds. This money cannot be used to issue new loans, so the growth of reserves may indirectly put pressure on the cost of loans. This is one of the factors that makes banks more cautious when changing loan conditions.

Переведено сервисом «Яндекс Переводчик»