In dry prosperity: deposit rates dropped below 14.5%

Average deposit rates have dropped below 14.5%, which is the lowest since the end of 2023, Izvestia found out. Over the year, they decreased by almost 7 percentage points following the key one. At the same time, banks include further easing of the regulator's policy in the cost of products. The annual deposit yield averages 13.5%. What will happen next with the rates and whether it is worth fixing the yield now — in the Izvestia article.

Deposit rates decreased in large banks

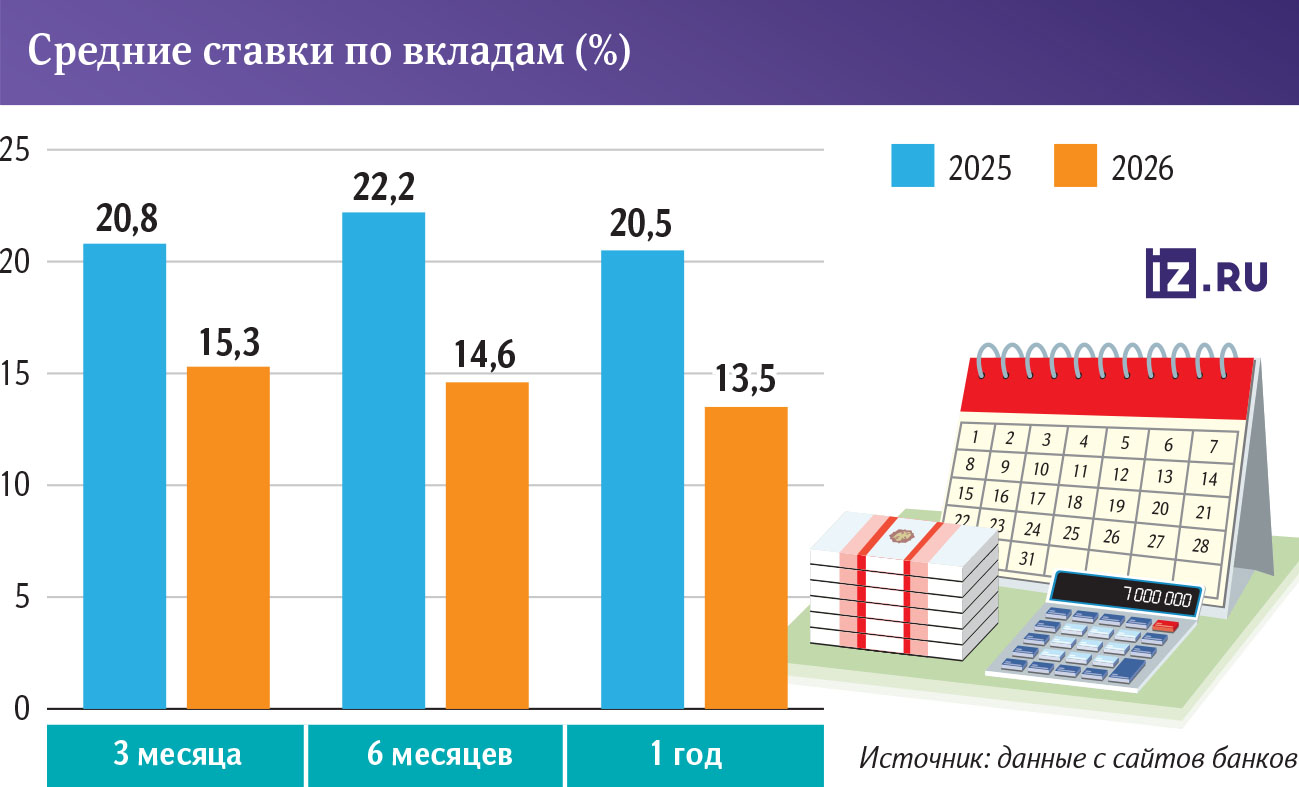

The average yield on deposits for a period of three to 12 months has dropped below 14.5% per annum, according to data from the websites of the ten largest banks that Izvestia studied. According to the Central Bank, the last time such modest values were only in December 2023, when the key value was also at the level of 16%.

In January 2025, average deposit rates reached 21.2%, Izvestia calculated. That is, the indicator decreased by about 6.7 percentage points over the year, while the key one decreased by only 5 percentage points over the same period.

— At the beginning of last year, banks often placed deposits above the key one as a share during a period of intense competition for customers and in anticipation of a further increase in the Central Bank's rate, — explained Ilya Vasilkov, head of the Deposits product at the Compare financial marketplace.

Now, credit institutions are adjusting the cost of their products with the expectation that the regulator's rate will continue to fall, said Vitaly Kostyukevich, director of Absolut Bank's retail products department. That is why the market focuses on deposits for short periods of time — no one expects that the key rate will remain at the current level even for six months.

Three-month deposits now average about 15.3% per annum, Izvestia estimates. For a six-month period, the average yield dropped to 14.6%, while banks offer only about 13.5% for deposits for a year.

By the end of 2026, the key rate will drop to 12-13%, and the average deposit rates for up to a year will reach 10-12%, predicts Finam analyst Igor Dodonov.

Izvestia sent a request to the Central Bank about the impact of citizens' savings activity on slowing inflation, and also asked the main market players for comments.

Should I open a deposit now

"There will be no significant changes in deposit rates by the end of the first quarter of 2026," said Natalia Milchakova, a leading analyst at Freedom Finance Global.

At the first meeting of the Central Bank on the key issue in 2026, which will be held on February 13, the regulator may take a break, the expert believes. In this case, banks will have no incentive to further reduce deposit yields.

At the same time, they will definitely not grow — if at the beginning of 2025, credit institutions actively fought for the client and tried to offer higher interest rates on deposits, now this should not be expected, explained Vitaly Kostyukevich from Absolut Bank.

With a decline in key deposit yields, they will inevitably fall, so customers will try to "jump into the last carriage." Banks will now have no problems with the demand for savings products — according to the Central Bank, at the beginning of November 2025, the volume of Russians' funds on deposits reached a record 63.5 trillion rubles. It increased by 6.2 trillion over the year.

The demand for customer funds in the market may grow in three to six months, when the validity period of the currently open short deposits expires, said the Deputy Chairman of the Board of Dom Bank.Russian Federation" by Alexey Kosyakov. Because of this, the bids may rise slightly due to promotional offers. However, a massive increase in yields should not be expected.

— Now it clearly makes sense to fix the current yields for the longest possible period, — said Igor Rastorguev, a leading analyst at AMarkets.

At the same time, savings can be divided into several parts, Igor Dodonov believes. According to the analyst, one should be put into long-term deposits in order to use the highest profitability. But for more flexibility, some of the money should be left on short deposits.

At the same time, the reduction in deposit rates gradually changes the balance between them and other instruments, Igor Rastorguev said. According to his estimates, the flow of funds into stocks and bonds will begin at a key rate of about 12-13%, when deposit yields will decrease even more.

Now it is also possible to pay attention to the purchase of federal loan bonds (OFZ) with a fixed coupon, Igor Dodonov noted. Investors are already actively investing in these instruments, the expert confirmed.

— The Russian stock market is experiencing a unique situation where real product yields (the rate minus inflation) are reaching historical records. Many investors are in a hurry to fix it," Finama clarified.

Long-term OFZs are already yielding about 14-15% per annum in the form of coupons, Igor Rastorguev noted. At the same time, investors expect to earn not only on coupon payments on bonds, but also on an increase in their value, which they will receive by the time they close. The total return on them can be 20-25% per year.

At the same time, it still makes sense to keep a significant share of funds on deposits — as long as the rates on them remain at a high level, Natalia Milchakova believes. Currently, it is still possible to find deposits in Russia at 15-16% per year — if you open it now, by January 2027, the investor will receive a decent real income against the background of the expected slowdown in inflation to 4-5%.

Переведено сервисом «Яндекс Переводчик»