Reduced cost: the average mortgage overpayment for the year decreased by a third

Mortgage overpayment decreased by a third on average over the year, Izvestia estimated. In November 2024, it was about 470% of the original loan amount, now the figure has dropped to 324%. This level is still too high — in fact, borrowers take one apartment for the price of four. At the same time, the demand for market mortgages has been growing in recent months — customers are entering into transactions in anticipation of a reduction in the key interest rate and the opportunity to refinance the loan in the future. Why people are willing to take out loans at 21% per annum is in the Izvestia article.

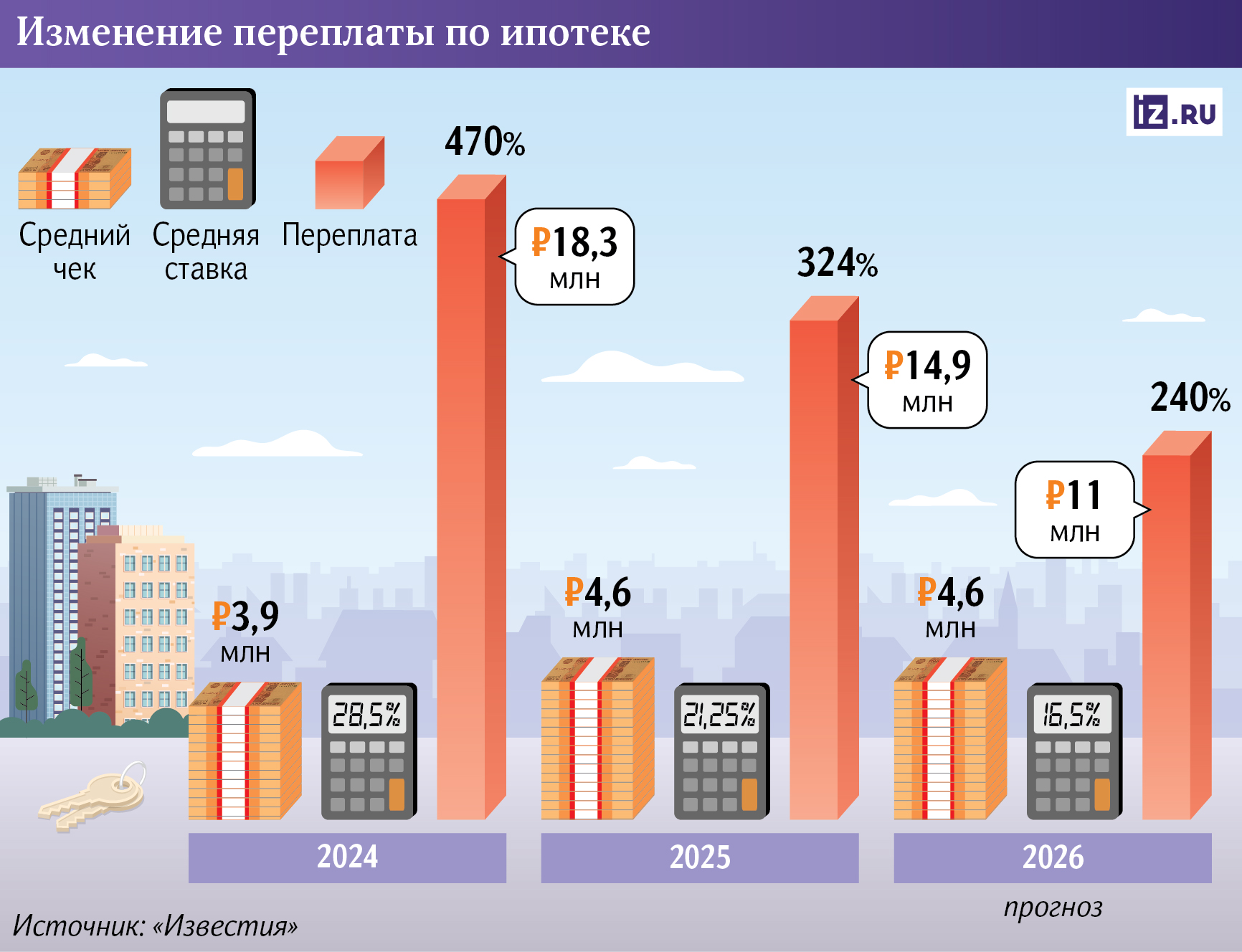

How much has the level of mortgage overpayments decreased

The average level of overpayment on a market mortgage in the Russian Federation has decreased by a third over the year, Izvestia estimates. If in November 2024, Russians on average overpaid 470% of the initial loan amount, that is, just under five apartments, then a year later the figure dropped to 324%.

The main reason is the decrease in market rates in the top 20 mortgage banks. In November last year, their average level, according to "Dom.Russian Federation", reached 28.5%. And in the same month of 2025, it has already dropped to 21.25%.

During this period, the average term of market housing loans decreased from 242 to 239 months, the United Credit Bureau (OKB) clarified. At the same time, the average size of mortgage loans increased slightly and in November 2025 amounted to 4.6 million rubles (compared to 3.9 million a year earlier), according to the Central Bank. Nevertheless, due to lower rates, the overpayment has significantly decreased.

With such conditions as in November of this year, the overpayment on the mortgage could amount to about 15 million rubles, follows from the calculations of Izvestia. A year earlier, it reached about 18.3 million rubles.

— The reduction in overpayment can be called significant. But "substantial" here does not mean "comfortable" for the family budget — it's just that the market has moved from a very extreme level to less harsh conditions," stated Vladimir Chernov, analyst at Freedom Finance Global.

In any case, this level is too high — now the borrower pays for more than four apartments, but actually gets only one, said Ivan Uklein, Senior Director for Bank Ratings at Expert RA.

In addition, it is often necessary to insure real estate and health when applying for a mortgage, Valery Tumin, Director of the Russian and CIS markets at fam Properties, recalled. Over the entire payment period, contributions can increase the borrower's total costs by 5-10% above the percentage overpayment.

At the same time, in the first years of the loan, in most cases, the payment covers 80-90% of the accrued interest, said Vitaly Kostyukevich, director of Absolut Bank's retail products department. That is, at first, the borrower mainly pays for the additional profit of the credit institution and only towards the end of the mortgage term — the value of the property itself. Therefore, the total amount strongly depends on the size of the rate in the first years after the loan is issued.

Why do people take out mortgages at prohibitive rates

The Central Bank notes a 30% increase in market mortgage issuance in the third quarter compared to the previous one. Borrowers reacted to the reduction in interest rates, which dropped after the key one. In October, it was 16.5%.

— Now those who delayed the deal for a long time have gone to the banks. Credit institutions have collected pent—up demand from customers who were waiting for the key rate cut to begin," said Alexey Popov, chief analyst at Cyan.

Mortgages at current rates are issued either because of the urgent need to improve living conditions, or for the sake of buying real estate at a discount in order to fix a lower price, said Regina Dydalina, executive director of the federal company Floors. Many people believe that it is risky to wait for a reduction in rates: during this time, the discount may disappear, and prices for good apartments may rise sharply.

— In any case, loans at such high interest rates are very rarely taken with an eye to paying over a long period of time, — Alexey Popov added.

Now the majority of those who apply for mortgages at market rates immediately contribute most of their own funds — from 50% and above, explained Regina Dydalina. Individual borrowers plan to partially repay the loan ahead of schedule after the sale of existing real estate.

In addition, Russians expect to refinance the mortgage that they took out at exorbitant rates, that is, to apply for a loan on new terms in order to reduce their debt burden. Banks are already recording an increase in demand for such procedures, as confirmed by VTB and Dom Bank.RF", PSB and Sovcombank. Izvestia has sent inquiries to other market players.

Reducing average mortgage rates from 28.5% to 21.25% reduces the monthly payment by about a quarter, explained Vitaly Kostyukevich from Absolut Bank. The amount of the overpayment is also decreasing, so refinancing already makes a lot of sense.

At the same time, the process cannot be called easy, emphasized Vladimir Chernov from Freedom Finance Global. During refinancing, the bank actually re—issues a loan to the borrower - it checks his income, debt burden, credit history, evaluates the object, charges fees for assessment and insurance. For some borrowers, the associated costs can simply "eat up" the benefits.

— Refinancing is economically beneficial if the new mortgage rate is about 3 percentage points lower than the current one, — concluded Vladimir Chernov.

At the same time, by the end of 2026, the key rate may drop by 4.5 percentage points, to 12% - this corresponds to the forecasts of the Central Bank. This level, for example, is expected by the head of Sberbank, German Gref. In this case, the demand for mortgage refinancing may also increase.

If the key rate drops to 12% and mortgage rates fall below 17%, the level of overpayment on housing loans may decrease to about 240%, Izvestia estimates. This is another 25% lower than current levels.

In general, the demand for market-based housing loans will grow in 2026, Absolut Bank expects. An important role may be played by tightening the conditions for a family mortgage — its rates for families with one child may double to 12%. The authorities are currently discussing such a change.

In this case, borrowers can pay attention to the secondary housing market, where prices are still lower and locations may be more convenient. Prices for this segment of real estate will respond to the growing demand. According to Vitaly Kostyukevich, in the future, after a reduction in the key rate, they can catch up with the cost of new buildings.

Переведено сервисом «Яндекс Переводчик»