The burden of reckoning: Russians' loan debts have grown at a record pace in a year

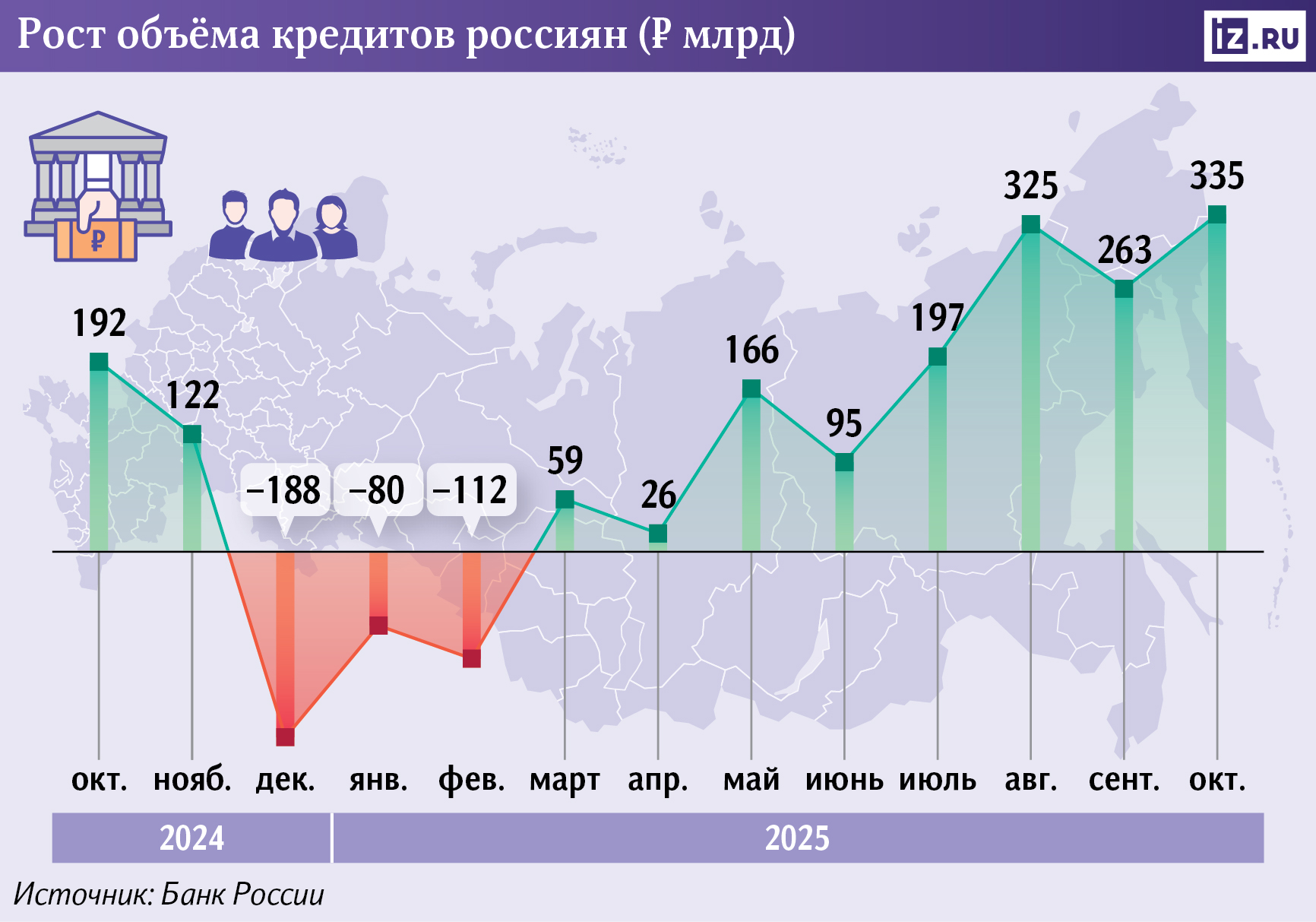

Household loan debts have jumped at a record pace over the past year, rising by 335 billion in October. Despite the fact that the key is still at a high level, pent-up demand is accumulating. Therefore, even with a slight reduction in the rate, people began to take out new loans. In addition, Russians actively applied for mortgages before the possible tightening of conditions under the family program. The total volume of loans to the population exceeded 38 trillion. Whether there are risks of high creditworthiness of citizens and whether the availability of borrowed money will increase next year is in the Izvestia article.

Why have Russians' borrowing debts jumped?

The total volume of loans to Russians in October jumped by 335 billion rubles, to 38.3 trillion, according to data from the Central Bank, which was analyzed by Izvestia. This is a record year—on-year increase since September 2024. The credit activity of citizens increased, despite the fact that the key was still at a very high level. On October 24, the Board of Directors of the Bank of Russia lowered the rate from only 17% to 16.5%.

This is due to accumulated pent—up demand - so far the Central Bank has kept the key rate at a record high. Demand was driven by even a slight reduction in bank rates and expectations of a shift to a softer monetary policy, explained Denis Astafyev, fund manager and founder of the SharesPro fintech platform.

Another reason for the growth was the reduction in banks' allowances for high-risk loans from September 1, said Dmitry Dolzhenko, Head of Consumer Lending Development at Ingo Bank.

At the same time, of the 335 billion rubles, the vast majority — 289 billion rubles — were secured mortgage loans, Dmitry Gritskevich, head of Banking and Financial Market Analysis at PSB, drew attention. First of all, there was increased interest in the family program due to the expected tightening of its parameters, in particular, the possibility of taking out only one preferential mortgage per family, he said.

The auto segment grew by 93 billion rubles in October, according to a report from the Central Bank. This trend is associated with a significant increase in recycling, Dmitry Gritskevich added. At the same time, unsecured loans, on the contrary, continue to decline, Denis Astafyev noted.

In the Dom bank.Russian Federation" demand for consumer loans increased in October by 10% compared to 2024, the credit institution noted.

The total amount of debt owed by Russians from January to October 2025 increased by only 1.49 trillion rubles, the lowest figure in the last eight years, according to data from the Bank of Russia. For comparison, over the same period last year, the loan portfolio of the population increased by 4.86 trillion rubles, and in 2023 — by 5.7 trillion. In addition, even in 2022, when the Central Bank raised the key rate to a comparable level (20%), the indicator increased by more than 2 trillion.

This dynamic indicates a sharp monthly surge in October, rather than a surge in mass lending this year, Denis Astafyev explained.

When will loans become more affordable in Russia?

Izvestia asked the Central Bank whether the regulator sees risks in a jump in Russians' loan debts.

From the point of view of inflation, the rise of 335 billion in October does not look dangerous yet — the annual growth rate of lending remains moderate, said Denis Astafyev from SharesPro. Point pressure is possible in the segment of housing and cars, but the economy does not demonstrate "credit overheating".

At the same time, there is a threat of high creditworthiness among the population, says Oleg Abelev, head of the analytical department at the Rikom-Trust investment company. In his opinion, this is evidenced by the increase in overdue loans from citizens — it has been increasing for two quarters in a row.

Against the background of a decrease in the quality of consumer loans and stricter requirements for borrowers by banks, there is a certain flow of borrowers to MFIs. In some cases, this may lead to an increase in their creditworthiness, according to the Central Bank's material, prepared on the basis of BCI data.

The problem is not so serious yet, Denis Astafyev believes. According to him, there are risks of over-crediting individual households, but the regulator systematically restrains them through a number of measures.

Due to this, in the first half of 2025, the debt of borrowers with three loans or more decreased by 0.4 trillion to 18 trillion rubles, according to an analysis by the Central Bank. However, they still account for about half of the total debt.

Currently, the availability of loans for the population is still low. It is limited by high interest rates and the strict conditions of banks for approving loan applications.

The availability of borrowed money will increase only when the incomes and well-being of the population will grow more significantly than they are now, independent expert Andrey Barkhota expects. This requires not only a reduction in the key rate by 2-3 percentage points next year, but also an increase in the number of jobs. Accordingly, this will happen at the very best at the end of 2026, he concluded.

We should not expect a massive credit boom next year: unsecured retail will remain under regulatory restrictions, Denis Astafyev suggested. After reducing the key rate, loans will become more affordable, but less affordable in terms of requirements for the borrower, Oleg Abelev added. However, the moderate debt growth will continue due to the accumulated demand for large purchases.

Переведено сервисом «Яндекс Переводчик»