The sum is worth it: Russians owe a record 20 trillion for a mortgage

The amount that Russians will have to pay on their mortgage loans has reached 19.7 trillion rubles, according to the Central Bank at the beginning of September. And this is the maximum value reported by the regulator. At the same time, in August, banks approved twice as many mortgage loans as at the beginning of the year. Among the reasons is the improvement of the borrower's "portrait": many of them have accumulated funds for the purchase of real estate and are ready to make a larger initial payment.

Banks have become more likely to approve mortgages

In August 2025, banks approved twice as many mortgage loans as at the beginning of the year, the Central Bank's press service told Izvestia. This may be due to an increase in demand for loans, as well as other factors, the regulator believes.

"For example, even after a slight decrease since August 1, the amount of compensation to banks under the Family Mortgage, Far Eastern Mortgage and Arctic Mortgage programs remains increased," the Central Bank explained. "Also this year, we have reduced macroprudential surcharges three times (additional capital requirements for banks when issuing certain categories of loans. — Ed.) on new mortgage loans. And now there are no surcharges for loans with acceptable risk characteristics in mortgages for the purchase of housing under construction: an initial payment of 20% and a borrower's debt burden of no more than 70%."

Against this background, the total volume of mortgage loans to Russians has increased by 500 billion since the beginning of the year and reached a record 19.7 trillion rubles by September, according to Central Bank data analyzed by Izvestia.

In August, Russians issued mortgage loans worth 392 billion rubles. This is 5% more than in the same month of the previous year. This figure has tripled compared to January 2025.

Dom.RF Bank also confirmed an increase in demand for a standard mortgage without government support.

— Clients apply for such loans against the background of expectations of lower interest rates with the expectation of refinancing later on more favorable terms. In July, the share of market mortgages in issuance was 10%, compared to less than 1% at the beginning of the year," said Alexey Kosyakov, Deputy Chairman of the bank's board.

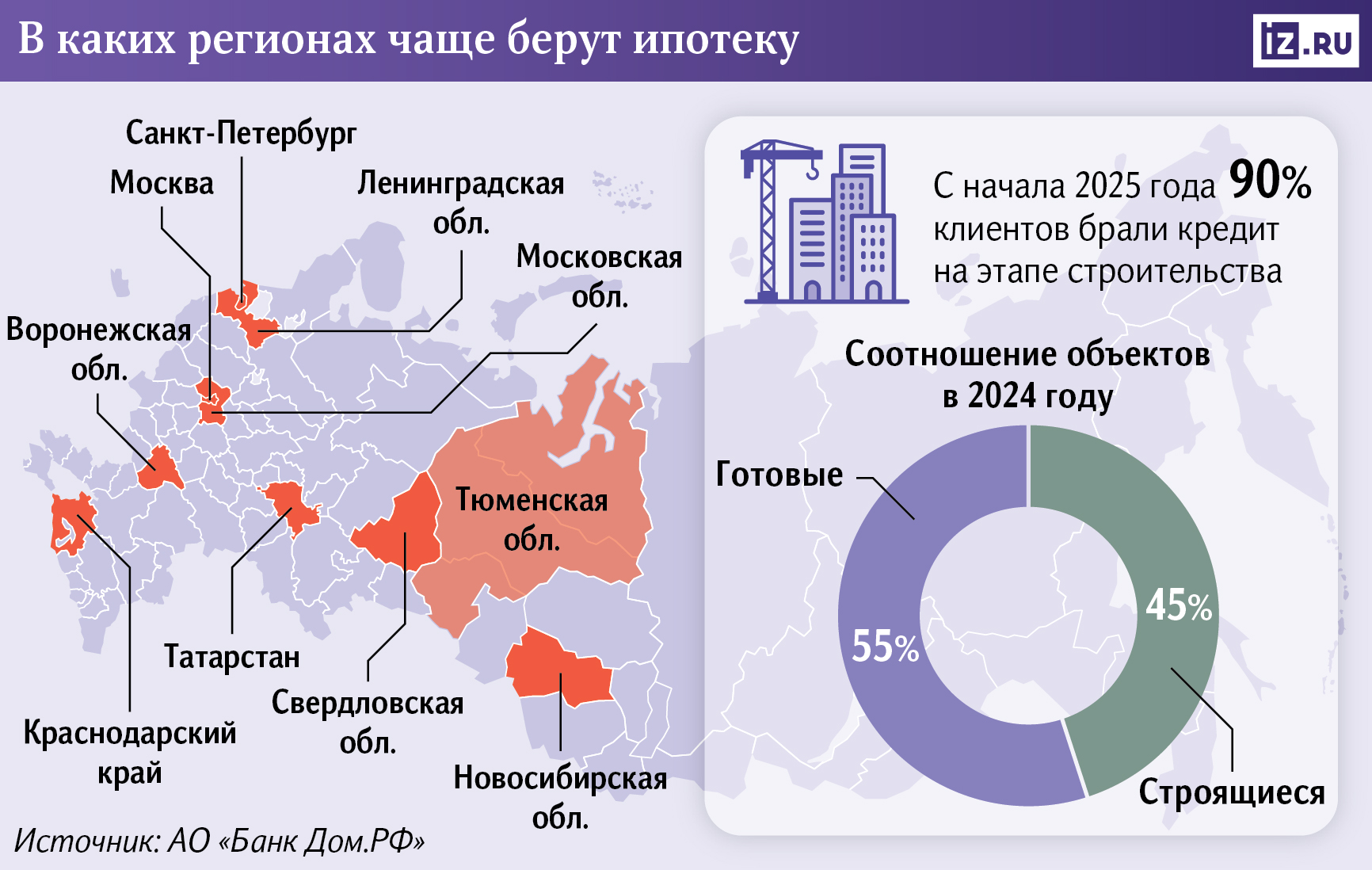

90% of clients took out a loan to purchase a home during the construction phase. Last year, this figure was 45%, while the rest of the borrowers bought houses that had already been built. Most often, loans without government support were issued by residents of Moscow, the Moscow region, St. Petersburg, Tyumen, Sverdlovsk, Leningrad, Novosibirsk, Voronezh regions, Tatarstan and Krasnodar Territory.

Banks have relaxed their requirements for mortgage borrowers, real estate market participants have also confirmed. According to the Mangazeya development company, the share of approved applications has increased by 30-35% since the beginning of the year.

"After a period of caution, creditors began to evaluate the real possibilities of their clients more carefully," said Yulia Arkhangelskaya, head of the Commercial services department at the development company. — The number of unmotivated refusals decreased when the questionnaire formally met all the requirements. Today, reliable borrowers receive approval almost instantly, and the speed of transactions has increased significantly.

According to her, certain difficulties still remain for entrepreneurs and the self-employed. Banks still classify them as high-risk due to possible income fluctuations. These clients take about a third longer to check their documents than employees. However, with stable revenues and transparent reporting, the chance of a positive decision remains high.

Why are loans being approved more often?

There has indeed been a noticeable recovery in housing mortgage transactions, analysts at the M2 real estate ecosystem have confirmed. Thus, the number of transactions in September increased by 43% compared to September last year and by 5% compared to August.

Almost every fourth transaction on the market is a mortgage transaction, experts have calculated based on Roskadaster statistics. At the same time, more than 490 thousand real estate transactions were registered in the EGRN in September. This is 4% more than a month earlier, and 1.3% less than in September last year.

— The main reason for the dynamics in mortgage transactions is seasonality. There are more working days in September than in August," said Dmitry Smirnov, head of the M2 Analytics and Data Department.

Dmitry Sofronov, Commercial Director of DARS Group, noted that the share of mortgage transactions in the purchase of new buildings remains high — about 70-80%. Most of it is accounted for by family mortgages.

"After reports of possible changes in this program, customers began to apply noticeably more actively, trying to get a loan on current terms," he added.

Approval began to grow rapidly after lower deposit rates, as funds from bank deposits began to return to the real estate market, says Denis Zhalnin, CEO of the People development company. A higher share of the initial payment when applying for a mortgage for banks eliminates their risks, and therefore makes a more loyal approach to potential borrowers.

Now banks have become more loyal to repeat applications: if they could refuse earlier without explaining the reason, now they issue recommendations, after which they can be approved, added Regina Dydalina, executive director of the federal company "Floors".

"For example, some potential borrowers need to close previously issued credit cards or lower their limits, while others need to at least partially repay some loans or attract a co—borrower," she said. — Previously, the share of applications for which banks were ready to review again after improvements was at the level of 5%, but now it has doubled.

According to the expert, the Central Bank's reduction in the key interest rate has attracted borrowers with stable incomes to the market, who have a higher chance of loan approval and refinancing in the future, which also affects the growth in the approval rate of applications.

What to expect in the mortgage market

The most difficult period associated with a reduction in the share of mortgage transactions occurred in January 2025, when, due to the high interest rate on market mortgages, banks charged developers a high commission for issuing loans, Gulsina Shakova, head of the mortgage lending Department at Precisely Group of Companies, recalled.

"The situation returned to normal in the spring after the key rate cut," she said. — The fees have decreased significantly, and by the summer, some banks had canceled them altogether. This led to a sharp increase in demand: during this period, the volume of mortgage sales increased by about four times compared to January. The market share of mortgages, which was close to zero at the beginning of the year, reached 10%.

The average loan size in user requests throughout 2025 remains at about 4 million rubles, which is explained by the predominance of mortgage applications for the purchase of secondary housing, said the head of the expert analytics department of the financial marketplace "Banks.<url>" by Inna Soldatenkova.

"Given the high key interest rate and current macroprudential constraints, most banks will continue to strive to provide mortgages only to high—quality clients with low debt loads," she said. — In addition, the observed increase in overdue mortgage debt does not contribute to the weakening of banks' credit policy.

The overall increase in withdrawals suggests that, although rates have not become fully acceptable or market-based, people have begun to get used to them and realize that there will be no sharp decline, says Svetlana Pinigina, founder of Pinigina Consulting.

— However, this growth cannot be called a record, — the expert noted. — Rather, the accumulated demand from those who postponed the purchase in anticipation of improved conditions began to be realized. In general, if the soft monetary policy continues and without serious macroeconomic shocks, mortgage demand will be moderate by the end of the year, with a slight seasonal increase.

However, it is not worth waiting for a repeat of the surge, as at the end of 2023, Pinigina added.

— I believe that the real growth may be about 20% if demand in November–December exceeds the September figures, but no more, — said the expert.

If the key rate reduction trend continues, the share of requests for standard mortgage programs will grow by the end of the year, said Alexey Novikov, Est-a-Tet's Chief Operating Officer.

Переведено сервисом «Яндекс Переводчик»