- Статьи

- Society

- Forbidden lot: family mortgage is not available to residents of almost half of the regions

Forbidden lot: family mortgage is not available to residents of almost half of the regions

The state program "Family Mortgage" remains practically inaccessible to residents of almost half of the country's regions, Izvestia found out. Experts of the center "Analytics. Business. Law" studied the average income of families in the constituent entities of the Russian Federation, current restrictions on loans, real estate prices and rates. And we found out that in 41 regions — for example, in the Crimea, Krasnodar Territory and Kaliningrad region — the average family cannot comfortably service a mortgage loan for the purchase of an apartment of 50 sq. m. The reason is the imbalance of housing prices and average family incomes, as well as the limitation of the amount of loans. How the situation with preferential mortgages will develop is described in the Izvestia article.

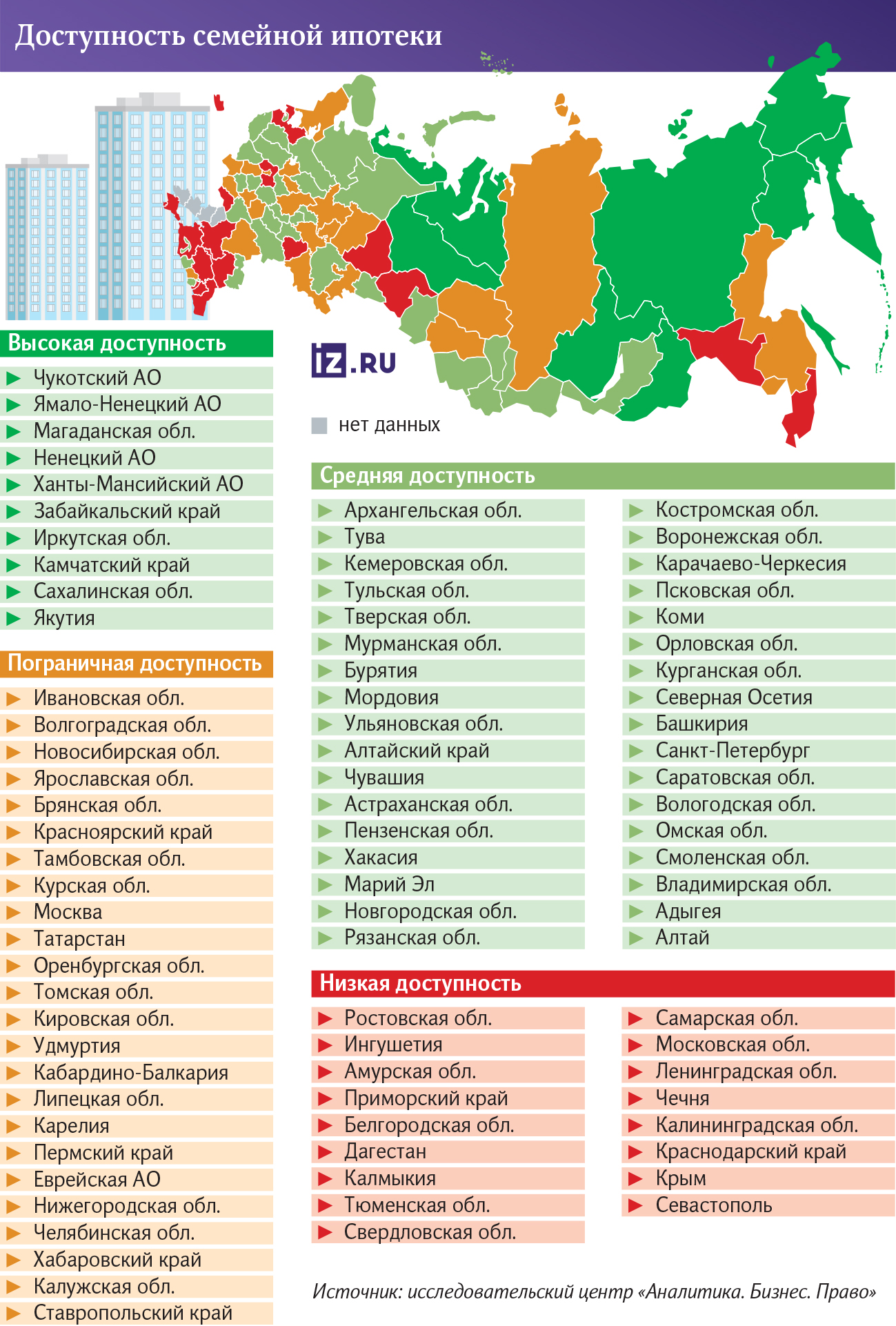

In which regions are family mortgages unavailable?

Residents of almost half of the country's regions cannot afford a family mortgage. This is the conclusion reached by the experts of the center "Analytics. Business. Pravo", having studied the data of the Ministry of Construction on the cost per square meter of housing for the second quarter of 2025 and Rosstat statistics on average salaries in the regions for 2024. Calculations have shown that in 41 regions of Russia out of 89, an average-income family is unable to comfortably service a mortgage for the purchase of a 50-square-meter apartment.

In regions where housing prices are disproportionately high compared to salaries, there is the least availability of mortgages, analysts said. For example, in the Krasnodar Territory, Kaliningrad Region and Crimea, where the cost per square meter has grown significantly faster in recent years than salaries.

"The current restrictions, 6 million rubles for most regions, also create difficulties due to the high cost of housing," said Venera Shaidullina, director of the research center. — For example, in the Krasnodar Territory, the average cost of an apartment is 50 sq. m. The loan amount is about 9.6 million rubles, which significantly exceeds the loan limit, forcing borrowers to make a substantial down payment.

Sevastopol, Primorsky Krai, Belgorod, Amur, Rostov, Leningrad, Moscow, Samara, Sverdlovsk and Tyumen regions, Chechnya, Dagestan, Ingushetia, Kabardino-Balkaria and Kalmykia were also among the subjects with the lowest availability of such loans.

— The analysis showed a significant gap in mortgage availability between regions. These are subjects with too high housing prices," said Venera Shaidullina. — Or economically developed regions with an imbalance of prices and incomes, like the Sverdlovsk region. The list also includes subjects with low salaries.

Analysts have divided the availability of family mortgages by region into several categories. A high one, where, despite the cost of housing, a high salary level allows you to comfortably service mortgage loans. Medium — the loan is available to middle-income families, although mortgage payments make up a significant part of the budget. Borderline, meaning families have to spend a little more than 30% of their income on payments. And low — the purchase of housing using a preferential loan is almost impossible without additional sources of financing.

State-backed mortgages proved to be the most affordable in the northern and Far Eastern regions with high salaries: in Chukotka, the Nenets, Yamalo-Nenets and Khanty-Mansi Autonomous Okrugs, and the Magadan Region. In regions with a good ratio of wages and housing prices: the Trans-Baikal Territory, the Irkutsk Region and Yakutia. And regions with special economic conditions: Kamchatka and Sakhalin.

Why is it difficult to get a family mortgage

In the south of Russia, the situation is complicated by the peculiarities of the market, experts say. Krasnodar Territory, Crimea and Sevastopol are traditionally attractive for relocation, so prices here are driven up not only by local demand, but also by the influx of buyers from other regions, said Igor Rastorguev, a leading analyst at AMarkets. At the same time, the average incomes of the population of the southern regions remain lower than in Moscow or St. Petersburg, which leads to an imbalance.

"However, even in the capitals, accessibility is limited: the cost of housing in Moscow and St. Petersburg significantly exceeds the national average, and even above—average incomes do not always allow a family to painlessly service a long—term loan," the expert added.

At the same time, family mortgages remain a driver of the development of the construction industry, as market rates are significantly higher and inaccessible to most citizens regardless of the region of presence, believes Vladimir Prokhorov, member of the General Council of Delovaya Rossiya, developer, owner of Udacha Group of Companies.

The reason for the current situation is an economic imbalance, said Dmitry Vladimirov, managing partner of the IDI—Project project company. The program is highly accessible in regions where high incomes of the population are combined with an adequate cost per square meter.

— There are not so many of them, considering that over the past five years, new buildings in the country have risen in price at least 2-2.3 times, — he said. — As a result, in a number of regions there really is a situation where low incomes of families simply do not allow them to save for the down payment and service the family mortgage.

If you take an apartment with an area of 50 square meters, then in Moscow such real estate will cost an average of 13-16 million rubles, in Russia — 9-10 million rubles, explained Evgeny Shavnev, CEO of Flip LLC, an investment company in the real estate market.

— Prices vary greatly from region to region. However, the average price per square meter in Russia is about 200 thousand rubles," he said. — If we consider a 20-year mortgage under a preferential program with a down payment of 20%, then the monthly payment will be at the level of 50-55 thousand rubles. This is 50% of the nominal salary in Russia. At the same time, we understand that if we are talking about a family mortgage, then quite often there is only one working person in the family, and this is a significant burden on the family budget.

Recently, the number of refusals to grant preferential loans has increased, confirmed Vladimir Chernov, analyst at Freedom Finance Global. Among the reasons are the tightening of banking internal standards after macroeconomic instability, a high proportion of "gray" salaries, insufficient initial payment, poor credit history, high debt burden and non—compliance of real estate requirements.

An increase in approvals is possible with a further reduction in interest rates, an increase in real incomes of the population, a softening of the parameters of banking practices such as flexible scoring (a system for assessing a person's creditworthiness), and the adaptation of joint risk programs with the government.

How can the situation be improved

To make family mortgages available in more regions, it is advisable to adjust the program parameters, Igor Rastorguev believes. For example, additional regional adaptations may be considered, especially for southern resort regions and economically developed areas with high housing costs.

— In regions with high housing costs, the existing limits of 6 million rubles are not enough to buy an apartment of medium size, — added Venera Shaidullina. — Increasing the limits could increase the availability of programs. And in low-income regions, such as the republics of the North Caucasus, additional support measures can be considered to increase housing affordability.

In addition, analysts believe, it is necessary to balance measures to increase the availability of mortgages with the risks of overheating the real estate market, especially where there is already a significant increase in prices.

If the program is extended in the current format, and the situation on the housing market in terms of prices does not change, it is possible that the trend will continue, and the regional imbalance will increase, Dmitry Vladimirov added.

— To fix the situation, we need a targeted, differentiated approach. One of the options, which, by the way, has already been proposed, is the introduction of a differentiated interest rate on a preferential mortgage," the expert recalled. — To offset the regional imbalance, it might help to link the terms of the program — be it the amount of subsidies, the maximum cost of housing or the amount of benefits — to income and the cost per square meter in each specific region.

According to Vladimir Prokhorov, the introduction of a special type of housing, which is sold only under this mortgage format, can also improve the situation. It should not be freely available, but rather something like municipal housing, that is, it is limited in value.

"Of course, such a measure will limit borrowers in choosing a location, but it will solve the problem of family mortgage availability, as well as provide additional jobs in the construction sector in specific regions," he stressed.

It is also possible to reduce the required initial payment for families or introduce a minimum for part of the program quotas, expand the list of income to be confirmed and introduce more flexible thresholds for the maximum debt burden for families, extend the loan term to 25-30 years, Vladimir Chernov believes.

— It is possible to introduce targeted subsidies for low—paying regions or targeted subsidies for the initial payment, - said the expert. — Or to ease the liquidity requirements of collateral for the secondary market in depressed regions.

According to him, programs with targeted subsidies and expanded criteria can be implemented in the short term for 6-12 months, but a large-scale restructuring of the limits and a change in the structure of the housing market will take 1-3 years.

Переведено сервисом «Яндекс Переводчик»