- Статьи

- Society

- Installment payment under control: in Russia, from April 1, the rules for payment in installments will change

Installment payment under control: in Russia, from April 1, the rules for payment in installments will change

On April 1, 2026, Federal Law No. 283-FZ "On the Provision of Installment Payment Services" comes into force in Russia, which introduces uniform rules for the work of operators and sellers, sets time limits and penalties, and defines the procedure for transferring data to credit bureaus. Read more in the Izvestia article.

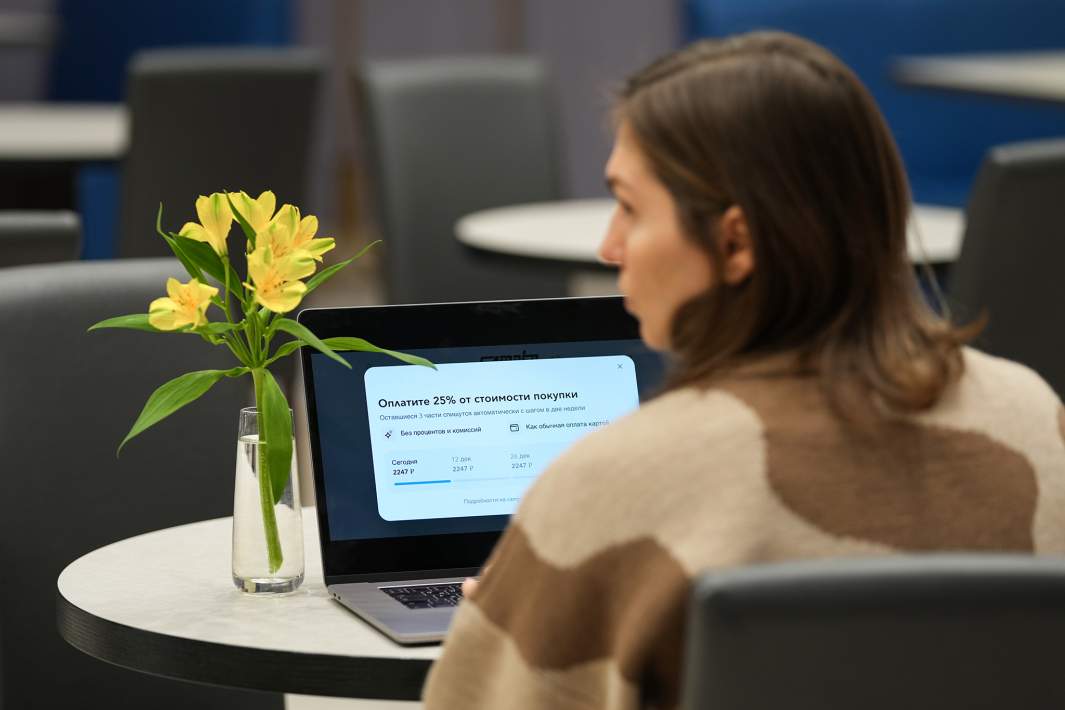

The price does not depend on the payment method

One of the main innovations concerns pricing. Now the cost of the product when buying in installments should be equal to the price when paying in full. Previously, sellers could set different price tags — lower when paying immediately and higher when using the installment service. Starting from April 1, this practice will be prohibited.

The terms of the interest-free installment plan are limited

Deadlines are set for interest—free installments through the operator: from April 1, 2026, the maximum period will be six months, and from April 1, 2028, no more than four months.

In turn, Anton Shmal, chairman of the Moscow Time of Protection Bar Association, clarified that installments for a period of more than one to two years are beyond the scope of the new law and will be considered as a consumer loan with the transfer of information to credit histories.

The limitation of the term of BNPL products (Buy Now, Pay Later — "buy now, pay later" — a method of paying for purchases in installments without interest and overpayments) is primarily necessary to distinguish between the usual loans and installments, experts say.

— The interest-free basis of installments should not create the illusion of free money for a long time, since increased deadlines are associated with increased risks for installment service operators. Installments are designed to stimulate public demand in retail outlets and marketplaces, but POS loans also perform the same function, which on a percentage basis allow you to use money for a period of more than six months," Vadim Krapp, a leading analyst on credit institution ratings at Expert RA agency, told Izvestia.

Such a period, according to Ekaterina Antonova, lawyer and chairman of the Antonova and Partners Bar Association, establishes a balance between the availability of small purchases and the need to control the debt burden of citizens.

— The limitation of installment periods is aimed at eliminating the substitution of marketing tools for loans. Long-term installments for a period of one year or more are economically a loan, which means they must be regulated by consumer lending legislation. In the new conditions, such products are likely to be transformed into classic credit instruments," Antonova said.

According to Anatoly Aksakov, chairman of the State Duma Committee on the Financial Market, such deadlines are due to statistics.

— Statistics show that the vast majority of installments are given for six months, no more. That is, this is a real practice in the market," Aksakov said.

Installments will be included in the credit history

The new law also introduces a threshold for the transfer of information to the Bureau of credit histories (BCI). If the amount of obligations to the operator exceeds 50 thousand rubles, the information is transmitted to the BKI. If the amount is up to and including 50 thousand rubles, the transfer obligation does not arise.

— The operator of the installment payment service cannot conclude an agreement with the client without transmitting information to the Credit History Bureau if the amount owed under all agreements exceeds 50 thousand rubles in total. The operator must identify the client in accordance with the law and transfer data to the BKI on all concluded installment agreements in order to issue amounts in excess of the limit of 50 thousand rubles," said Vadim Krapp.

At the same time, if the consumer takes several installments from one operator, they are summed up.

— For example, two contracts are concluded sequentially: in one contract, the cost of services is 30 thousand rubles, and in the other — 40 thousand rubles. If by the time the second agreement is concluded, the debt under the first one will be partially repaid and will amount to less than 10 thousand rubles (i.e. the total debt will amount to less than 50 thousand rubles), the information will not be transmitted to the BCI. If the total amount of debt exceeds 50 thousand rubles, the information will have to be transmitted," Yuri Vorobyov, partner of the Pepelyaev Group law firm, gave an example in a dialogue with Izvestia.

Penalties for late payment are limited

In addition, the new law limits the amount of penalties for non-fulfillment or improper fulfillment of installment obligations. Now the amount of penalties cannot exceed 20% per annum of the overdue debt amount.

— Previously, there were such fines that the buyer actually paid twice or even three times the price for the provided goods in installments. Moreover, it was necessary to pay the fine not from the amount that you owed, but from the entire amount of the goods taken in installments," recalls State Duma deputy Anatoly Aksakov.

Thus, the innovations are aimed at protecting consumers, easing their financial burden.

Additional services and commissions are prohibited

The new law introduces a complete ban on charging for additional services specified in the installment agreement. This means that installment service operators do not have the right to charge users a commission for providing installments, as well as for making payments.

However, the restrictions do not apply to other contracts that may be concluded with clients, such as an insurance contract.

— If the client has signed a separate agreement for the provision of additional services, the installment service operator may charge a fee for the provision of services. In this case, the installment agreement and the service agreement are not legally linked, while the law on installment services prohibits charging fees for the provision of services only under the installment agreement, — said Vadim Krapp.

Exceptions to the new law

The new law regulates only those installments provided by specialized operators.

— If the store independently offers the customer the opportunity to pay in installments without intermediaries, such relations are not subject to the new law and will be regulated by consumer protection legislation and the Civil Code of the Russian Federation. This may encourage sellers to use direct contracts without the participation of operators in order to avoid the application of new rules," explained Anton Shmal.

The question also arises whether the previously issued installments are still valid. According to Vadim Krapp, contracts concluded before April 1, 2026, will continue to operate on the same terms.

"Unlike lending, BNPL products do not have explicit refinancing programs, however, the installment service operator is free to meet customers halfway," the expert concludes.

— Contracts that have already been concluded remain in force and are not subject to automatic revision. This corresponds to the general principle of non-retroactivity of the law. At the same time, in the case of excessive penalties, consumers retain the right to reduce them in court as disproportionate to the consequences of violating the obligation," Antonova's lawyer added.

Requirements for installment service operators

The law also introduces the status of an installment payment service operator, a legal entity authorized to provide installments. Information about them will be recorded in the register of the Bank of Russia.

According to the new rules, operators are required to:

— have an equity capital of at least 5 million rubles;

— notify the Bank of Russia of the appointment of the sole executive body and provide information on the structure and composition of shareholders;

— submit accounting and other reports to the Central Bank from January 1, 2027;

— the rules for the provision of installments should be posted on the operator's website;

— transfer information about contracts worth over 50 thousand rubles to the BKI. rubles';

— record the facts of the conclusion of installment agreements and store information about them for five years.

At the same time, the operator is prohibited from combining the activities of providing installments with the activities of a non-credit financial institution, unless it is a microfinance organization.

Why do we need innovations?

According to Ekaterina Antonova, the adoption of the law on the regulation of installment services is a natural stage in the development of the consumer finance market.

"In recent years, installments have actually become an alternative to lending, but at the same time remained outside full—fledged legal control, which created risks for both consumers and bona fide businesses," she noted.

Experts also point to the social reasons for the innovations.

"Due to the fact that the population of our country is very heavily indebted, and the incomes of the population do not have time to increase in comparison with real inflation, the state wants to reduce the social burden," Jalil Mustafin, director of the Jalil Mustafin law firm, emphasized in a conversation with Izvestia.

The expert believes that the changes will prevent both over-crediting of consumers and bankruptcy of financial structures in case of non-payment by buyers.

Market implications

According to Deputy Anatoly Aksakov, the innovations will have a positive effect.

— This is, of course, a positive norm for buyers. Now they will purchase the product without additional charges and understand that they are not being misled. Consumers will be protected by a system of fines," he said.

The MP expressed the opinion that the bill would benefit not only consumers, but also businesses, as the new rules would increase confidence in sellers.

Ekaterina Antonova believes that innovations have both positive and deterrent consequences for consumers. On the one hand, they increase the transparency of installments and reduce the risks of abuse. On the other hand, the new law will reduce the availability of long—term installments, which may limit the possibility of purchasing expensive goods without attracting a loan.

For businesses, the expert believes, the new law means the need for a significant restructuring of sales models.

— Avoiding hidden fees and limiting installment periods will inevitably affect the average receipt and income structure. Nevertheless, the formation of uniform rules creates a more stable and predictable environment for the development of the market. And this is an absolute plus," Antonova said.

The expert also predicts the transformation of the market towards convergence with the banking sector: the development of hybrid products, the integration of installments into credit mechanisms, and the strengthening of the role of financial institutions.

"In general, regulation is aimed at increasing the transparency and financial stability of the system, even if this is accompanied by a decrease in its flexibility at the initial stage," Antonova summed up.

Переведено сервисом «Яндекс Переводчик»